Faster, safer, and more cost-effective transactions for businesses everywhere.

The financial world is changing, and at the heart of this revolution lies open banking. For years, merchants, both small and large, have faced challenges like high transaction fees, slow payment processing, and complex integrations. Open banking changes the game entirely. By allowing third-party providers secure access to financial data, open banking empowers businesses with faster payments, better customer experiences, and, most importantly, lower costs.

Table of contents:

1. Introduction to open banking

2. Open banking and A2A payments

3. Enhancing payment gateways with open banking

Improved transaction efficiency

Integration with existing systems

4. Challenges and considerations in adopting open banking

5. Future outlook: The evolution of payment gateways with open banking

Open banking is revolutionizing the financial landscape by enabling the secure sharing of financial data between banks, fintech companies, and other third-party providers through APIs. This innovative approach allows businesses to develop tailored financial solutions, streamline payment processes, and offer enhanced customer experiences.

As of 2024, the adoption of open banking has reached unprecedented levels. Globally, over 102 billion API calls were made, reflecting the rapid integration of open banking solutions across industries. Additionally, the total value of transactions processed through open banking systems surpassed $57 billion USD, showcasing its significant economic impact.

Open banking is a financial framework that enables the regulated sharing of customer data between banks and authorized third-party providers. It is designed to enhance the accessibility and functionality of financial services by allowing customers to securely share their banking information with other platforms they trust.

This framework operates through APIs, which act as digital bridges connecting financial institutions with fintech companies and merchants. APIs ensure that data is transmitted securely, eliminating the need for manual data entry or outdated methods of information sharing.

At its core, open banking provides businesses and consumers with:

What is the difference between open banking and A2A payments?

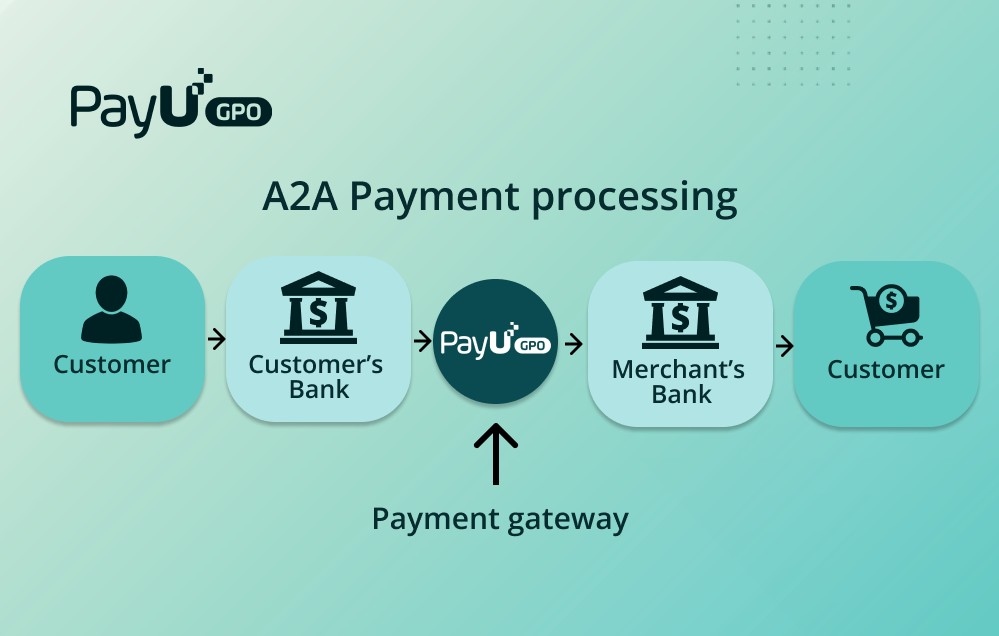

Open banking is a broader framework that enables secure data sharing and payment initiation, while A2A payments refer specifically to direct bank transfers between accounts without intermediaries like card networks.

Are A2A payments possible thanks to open banking?

Not always. A2A (account-to-account) payments and open banking are related but not the same. While open banking can enable A2A payments, A2A payments existed before open banking and can function without it. For example, Blik in Poland has existed for decades via traditional bank transfers, direct debits, or closed-loop bank partnerships.

Open banking driving A2A payments in emerging markets

Brazil is leading the way with Pix, its real-time A2A payment system, now integrated into the country’s Open Finance framework. This allows fintechs and merchants to accept instant bank payments through open banking APIs, reducing reliance on card networks. Similarly, in Nigeria, fintechs are leveraging the country’s newly established open banking regulations NIBSS to enable direct bank payments, making transactions easier for businesses and consumers.

South Africa’s PayShap is another step towards real-time A2A payments, with fintechs integrating open banking APIs to streamline the process. Meanwhile, Chile and Colombia are actively working on open banking regulations, which will further enhance A2A payment capabilities. In these markets, companies like Khipu (Chile) and PSE(Colombia) are expected to transition toward API-driven A2A payments as regulations take shape.

The Czech Republic is also making strides in this area, with its open banking ecosystem enabling fintechs and merchants to facilitate seamless A2A payments. Thanks to established APIs and increasing adoption by financial institutions, businesses in the Czech market can enhance payment efficiency while improving customer experience.

Open banking is transforming payment gateways, bringing a new level of efficiency, security, and integration to merchants worldwide. By leveraging open banking APIs, businesses can streamline payment processes and improve the overall customer experience.

One of the most significant advantages of open banking is its ability to facilitate direct bank-to-bank transfers. Unlike traditional payment methods that rely on intermediaries, open banking eliminates unnecessary steps in the payment process, reducing transaction times. Merchants benefit from faster settlements, ensuring cash flow is not delayed. Additionally, this streamlined approach significantly lowers transaction costs, a critical factor for businesses aiming to maximize their profit margins, especially small and medium enterprises (SMEs).

Security remains a top priority in the payment industry, and open banking addresses this concern with strong customer authentication (SCA). By requiring multi-factor authentication for each transaction, open banking minimizes the risk of fraud and unauthorized payments. Merchants can confidently offer open banking as a payment option, knowing that their customers’ data and financial details are protected. This enhanced security builds trust between businesses and their customers, fostering long-term loyalty.

Open banking APIs are designed for seamless integration with existing payment gateways, allowing merchants to enhance functionality without the need for costly overhauls. These APIs can be easily incorporated into a merchant’s current infrastructure, enabling additional features such as instant payments, real-time account balance checks, and better financial insights. This adaptability ensures that businesses of all sizes can adopt open banking solutions without disrupting their operations, paving the way for innovation and growth.

Through improved efficiency, robust security, and smooth integration, open banking is setting a new standard for payment gateways, helping merchants stay ahead in a rapidly evolving financial landscape.

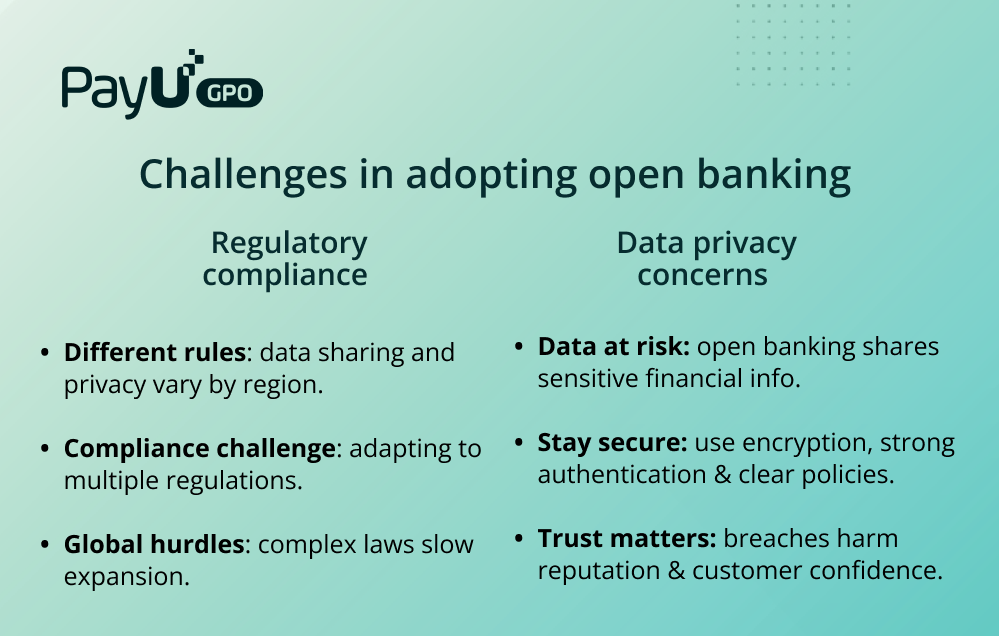

While open banking offers numerous benefits, its adoption comes with challenges and important considerations that businesses must address to ensure a smooth and secure transition.

One of the key challenges in implementing open banking solutions is adhering to regional regulations and standards. Different countries and regions have varying rules regarding data sharing, privacy, and financial transactions, which can create complexities for businesses looking to adopt open banking on a global scale.

Data privacy is another major concern when adopting open banking. Since open banking involves the sharing of sensitive financial information, it is essential for businesses to implement robust data protection measures to safeguard customer data. Strong encryption, secure authentication protocols, and transparent data usage policies are vital in maintaining the integrity of customer information. Any data breach or mishandling of personal data can severely damage a business’s reputation and customer trust. By prioritizing data security and following the best practices set by regulatory bodies, businesses can build a secure and reliable open banking environment.

As open banking continues to reshape the financial landscape, the future holds exciting possibilities. The integration of open banking into payment gateways is just the beginning, with several emerging trends set to further transform the way businesses and consumers engage with financial services.

One of the most significant developments in the future of open banking is the expansion into open finance. While open banking focuses primarily on sharing payment account data, open finance broadens this concept to include a wide range of financial products, such as insurance, pensions, and investments. This shift will enable customers to gain deeper insights into their financial profiles and access a more comprehensive suite of services.

The integration of more financial services into open banking ecosystems is expected to drive innovation. From lending and budgeting tools to wealth management solutions, third-party providers will have the ability to offer more diverse financial products, all based on secure, real-time data. The growing use of artificial intelligence (AI) and machine learning (ML) in financial services will further enhance the personalization of these offerings, tailoring financial solutions to individual consumer needs.

For businesses looking to stay competitive, adopting open banking solutions is not just a trend but a strategic necessity. Here are key recommendations for merchants considering the integration of open banking into their payment systems:

The evolution of payment gateways with open banking will continue to unlock new opportunities for businesses of all sizes. By staying ahead of emerging trends and adopting best practices, merchants can create a future-proof, customer-centric payment system that drives growth and fosters long-term success.

Open banking is transforming the global payment landscape, enabling businesses to provide more efficient, secure, and innovative financial services. By allowing the secure sharing of financial data through APIs, open banking facilitates direct bank-to-bank transfers, reducing transaction times and costs for merchants while enhancing security through strong customer authentication (SCA). This evolution in payment solutions is particularly beneficial for small and medium-sized enterprises (SMEs), offering cost-effective solutions and improved financial insights.

Looking to the future, open banking is expected to expand into open finance, allowing a broader range of financial services to be integrated into the ecosystem. Merchants can capitalize on this evolution by prioritizing compliance, investing in data security, and embracing flexible integration strategies. By adopting open banking, businesses can stay competitive, enhance customer experiences, and future-proof their payment solutions.