A2A is the broader concept of moving funds directly between accounts, while instant payments represent a specific method within A2A that ensures real-time settlement.

Benefits and implementation of direct bank transfers in payment solutions.

The digital financial services landscape is experiencing one of the most transformative periods in history. Fuelled by rapid technological advancements, digital payments have disrupted traditional financial systems, creating new opportunities while simultaneously presenting a range of challenges. This shift away from cash-based transactions is fundamentally reshaping how individuals and businesses interact with money, creating new opportunities for economic growth, financial inclusion, and social development.

Account-to-Account (A2A) payments are revolutionizing the way businesses and consumers handle transactions. By enabling direct bank transfers without intermediaries, they offer a faster, more secure, and cost-effective alternative to traditional payment methods. This article dives into the benefits of A2A payments, how businesses can implement them, and the innovations driving their future growth.

Table of contents:

Historical context and evolution

Integration with existing systems

Choosing the right payment gateway

Compliance and regulatory considerations

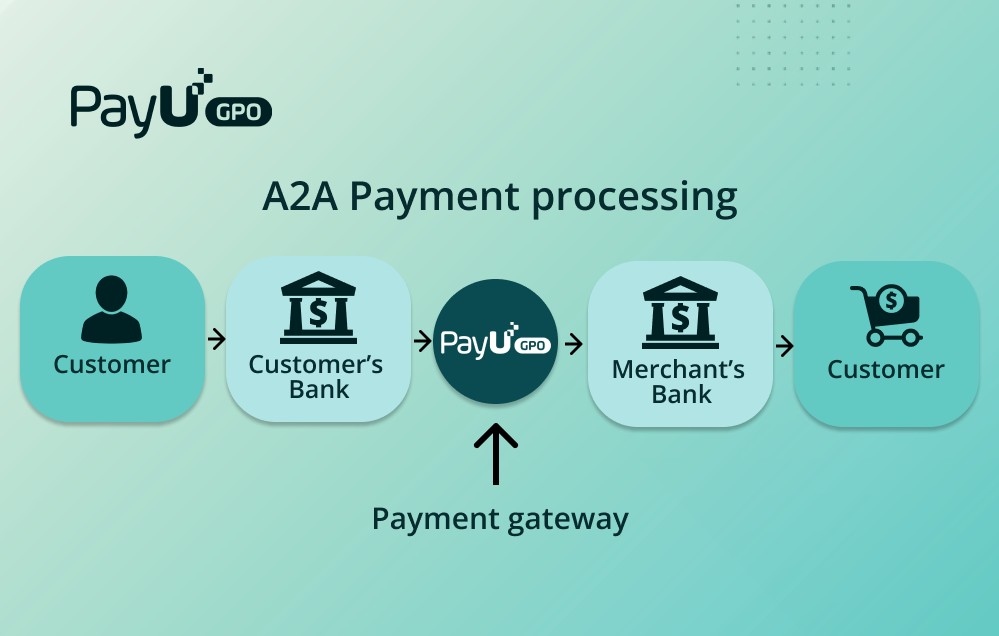

Account-to-Account (A2A) payments are a method of transferring funds directly between two bank accounts, typically via online banking systems or mobile apps. This method eliminates the need for intermediaries like payment processors or card networks, making transactions more cost-effective and efficient. With A2A payments, consumers can pay for goods and services directly from their bank account to the merchant’s account, without relying on traditional payment methods like credit or debit cards. This is particularly beneficial in countries where card adoption is not yet dominant, providing more payment options for consumers who may not have access to credit or debit cards.

Account-to-Account (A2A) payments refer to a direct bank transfer method where funds are transferred from one bank account to another without the involvement of intermediaries such as credit card networks. The key distinction between A2A payments and traditional card-based transactions lies in the role of intermediaries. While card-based payments rely on credit card networks and payment processors to authorize and settle transactions, A2A payments bypass these intermediaries, directly connecting the payer’s and payee’s bank accounts. This difference results in lower transaction fees, faster processing times, and reduced fraud risks. However, in markets like the United States, where credit card usage is deeply entrenched, A2A payments have yet to disrupt card-based transactions significantly. Many consumers still prefer credit cards for rewards programs, purchase protection, and credit-building benefits.

A2A payment apps are transforming the way people transfer money globally, with some standout examples leading the charge in their regions. In Brazil, PIX has become a household name, enabling instant, round-the-clock transfers directly between bank accounts using simple identifiers like phone numbers or QR codes. In Poland, Blik offers a seamless mobile experience with its innovative six-digit code system, widely used for in-store, online, and ATM transactions. India’s UPI (Unified Payments Interface) powers apps like Google Pay and PhonePe, providing real-time transfers across banks and revolutionizing payments. In Sweden, Swish is the go-to app for instant payments, backed by major banks and widely adopted for personal and business transactions. In Colombia, PSE, operated by ACH Colombia, serves as A2A payment method, allowing consumers to pay for goods, services, and bills without a credit or debit card. These innovations highlight how A2A payments are particularly transformative in countries where card infrastructure is underdeveloped, giving consumers a direct and efficient payment alternative.

The concept of A2A payments has evolved significantly over the past few decades. Initially, bank transfers were predominantly used for large-scale business transactions and often involved lengthy processing times and high fees. With the rise of the internet and digital banking, the process became more streamlined and accessible to both businesses and consumers. Early online banking services began offering customers the ability to make direct transfers, but these services were limited by slow processing speeds and security concerns.

The payment rail of A2A payments is a digital infrastructure that facilitates the direct transfer of funds between bank accounts without the need for intermediaries like card networks. These rails often leverage real-time payment systems (RTP) or clearing and settlement mechanisms provided by national or regional banking systems. Examples include SEPA Instant Credit Transfer in Europe, Faster Payments in the UK, UPI (Unified Payments Interface) in India, and ACH (Automated Clearing House) for batch processing in the U.S.

A2A payment rails rely on APIs, open banking protocols, and centralized clearinghouses or direct bank connections to process transactions seamlessly, making them a game-changer for both consumers and businesses.

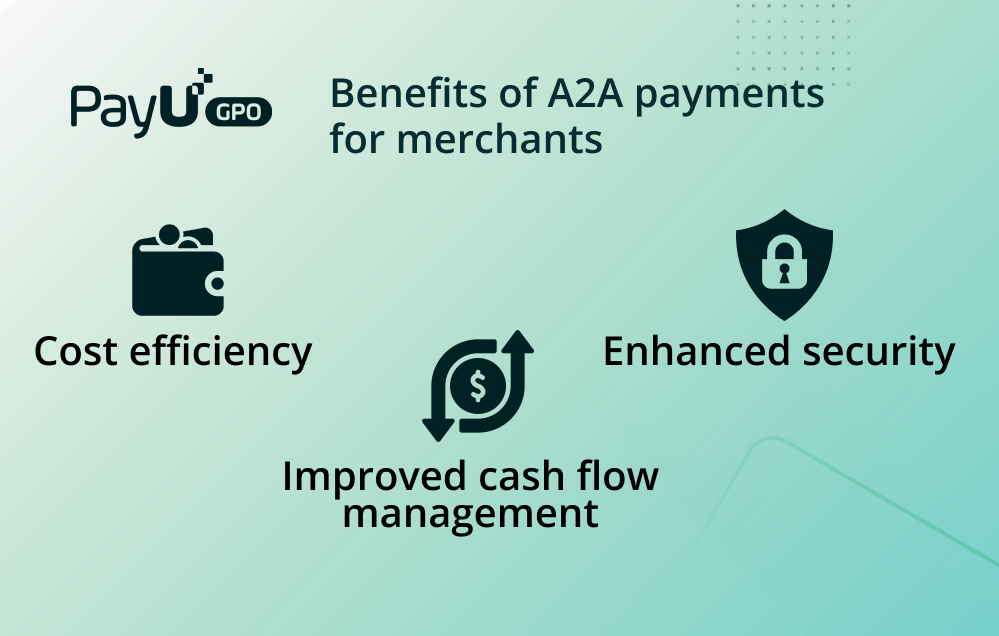

Account-to-Account (A2A) payments are a highly cost-efficient solution for merchants. Unlike card payments, which involve transaction fees for card networks, payment processors, and other intermediaries, A2A payments bypass these additional costs. By leveraging direct bank transfers, merchants can significantly reduce their payment processing expenses. This reduction in transaction fees directly translates into improved profit margins, enabling businesses to reinvest in growth initiatives or pass savings onto customers.

The security of A2A payments is another compelling advantage for merchants. These payments occur directly between bank accounts, leveraging advanced encryption technologies and secure authentication protocols. Features such as multi-factor authentication and tokenization ensure that transactions are safeguarded against fraud and unauthorized access. Compared to traditional card payments, which are more susceptible to fraud, chargebacks, and data breaches, A2A payments offer a more secure alternative.

A2A payments also contribute to better cash flow management for merchants by enabling faster settlement times. Traditional payment methods, especially card-based transactions, often involve delays due to intermediary processes and settlement timelines. In contrast, A2A payments ensure that funds are transferred directly and efficiently, with many transactions settling in real time or within a few hours. This rapid access to funds provides businesses with greater liquidity, allowing them to meet operational expenses, invest in inventory, and respond to market demands without unnecessary delays.

Implementing Account-to-Account (A2A) payments in your business can unlock significant benefits, but it requires a well-structured approach to ensure a seamless transition. From integrating A2A solutions into your existing payment systems to selecting the right payment gateway and navigating regulatory requirements, each step plays a crucial role in establishing an efficient and secure payment process. Here’s how to get started.

Integrating Account-to-Account (A2A) payment solutions into your existing payment infrastructure requires careful planning and execution. The first step is to evaluate your current system’s compatibility with A2A solutions, identifying any necessary upgrades or modifications. Once assessed, businesses can proceed with implementing APIs or software provided by the chosen payment gateway to enable direct bank transfers. Testing and monitoring are crucial during this phase to ensure seamless operation and address potential issues.

Selecting the right payment gateway is critical to successfully implementing A2A payments. Businesses should prioritize gateways that support real-time payments, offer robust security features, and ensure compatibility with their existing systems. Scalability is also essential, as it allows the payment gateway to grow with your business needs.

Adhering to legal and regulatory requirements is vital when processing A2A payments. Businesses must ensure that their payment solutions comply with local and international laws, including anti-money laundering (AML) regulations and know-your-customer (KYC) protocols. Data protection laws, such as GDPR in Europe or equivalent regulations elsewhere, must also be followed to safeguard customer information.

The future of Account-to-Account (A2A) payments is brimming with potential, driven by rapid technological advancements and growing market demand. As innovations like AI and blockchain transform the landscape, A2A payments are set to become more efficient, secure, and accessible. With projections pointing to significant global adoption, these payment systems are poised to redefine the way businesses and consumers transact in the years to come.

Emerging technologies are set to revolutionize Account-to-Account (A2A) payment systems, enhancing their efficiency and scalability. Artificial intelligence (AI) is already playing a role in streamlining transaction processes, detecting fraud, and personalizing payment experiences. Meanwhile, blockchain technology holds immense potential for A2A payments by enabling decentralized, transparent, and secure transfers, especially in cross-border scenarios. These innovations promise to make A2A payments faster, more secure, and widely accessible, solidifying their position as a preferred payment method.

The market for A2A payments is poised for significant growth, with experts predicting a sharp increase in adoption rates among consumers and businesses alike. As digital banking continues to evolve and open banking frameworks gain momentum, A2A payments are expected to become a cornerstone of global payment systems. This shift could reshape the financial landscape by reducing reliance on traditional card networks and intermediaries. In the coming years, the rapid expansion of A2A payments is likely to drive greater competition and innovation within the payment industry, benefiting businesses and consumers worldwide.

Emerging markets have become the true trailblazers in adopting A2A technology. With fewer legacy systems to overhaul, countries like Brazil and India have leapfrogged into the future with innovations like PIX and UPI, offering instant, 24/7 transactions. These solutions have driven financial inclusion, catering to unbanked and underbanked populations while reducing reliance on cash. The agility and necessity in these markets have made them prime hubs for A2A adoption, positioning them at the forefront of payment innovation.

Account-to-Account (A2A) payments enable direct transfers between bank accounts, eliminating intermediaries and reducing costs for businesses. These payments are highly secure, leveraging advanced encryption and authentication protocols, and offer faster settlement times, improving cash flow for merchants. Implementing A2A solutions requires integrating them into existing systems, selecting a reliable payment gateway, and ensuring compliance with financial regulations. Looking ahead, advancements in AI and blockchain are expected to enhance A2A payments, while market growth forecasts suggest they will play a central role in reshaping the global payment ecosystem.

Emerging markets have become the true trailblazers in adopting A2A technology. With fewer legacy systems to overhaul, countries like Brazil and India have leapfrogged into the future with innovations like PIX and UPI, offering instant, 24/7 transactions. These solutions have driven financial inclusion, catering to unbanked and underbanked populations while reducing reliance on cash. The agility and necessity in these markets have made them prime hubs for A2A adoption, positioning them at the forefront of payment innovation.

A2A is the broader concept of moving funds directly between accounts, while instant payments represent a specific method within A2A that ensures real-time settlement.

A2A is a payment solution, while Open Banking is the infrastructure and framework enabling broader financial innovation, including but not limited to payments.