What is JCB?

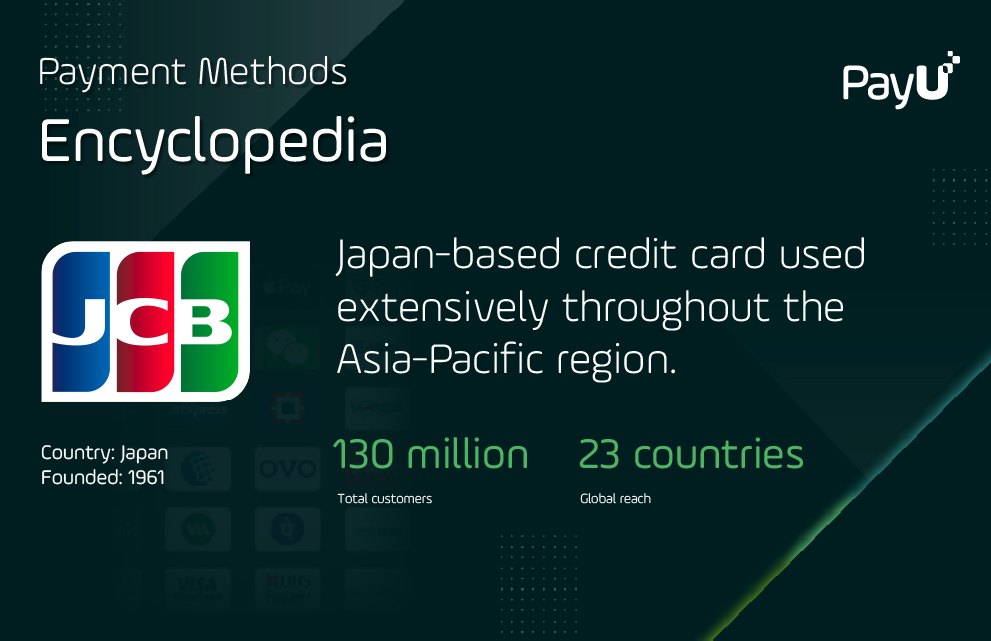

JCB (Japan Credit Bureau) is a credit card from Japan used by over 130 million customers in 23 countries throughout over the world. Founded in 1961, JBC continues to expand its business internationally and ensures that its cards function worldwide. This is a must-have payment solution for online merchants focused on the Japanese or Hong Kong e-commerce markets.

The majority of JCB cardholders live in the Asia Pacific region, including Japan, Hong Kong, China, South Korea, and Taiwan.

How does JCB work?

Consumers can use JCB cards online in the same way as credit and debit cards from major international payment networks. Once they reach the checkout, cardholders enter their card number, expiry date, and the CVV2 security code. The card and balance are instantly checked, and they get a payment confirmation within seconds.

To lower fraud risks further, JCB recommends using its 3D-Secure service (similar to MasterCard SecureCode and Verified by Visa). JCB merchant fees are charged as a commission (percentage).

Why do merchants and consumers use JCB?

Every online business should consider accepting credit cards as a form of payment to maintain a good cash flow and boost sales. Credit card acceptance can also help legitimize an e-commerce business and make it more competitive in the local market. Displaying the logos of the accepted credit cards is bound to attract the cardholder’s attention and make them more likely to trust your business. Accepting credit card payments also helps merchants to reach a larger number of customers and increase sales.

Credit card transactions are fast and convenient for both the customer and the business owner. The money is deposited directly into the merchant’s business’s bank account by the credit card processor within a matter of days. This will improve the cash flow while reducing problems with bounced checks or collection issues with customers.

With over 25% of all Japanese transactions being paid with JCB, supporting this payment method is crucial for merchants wanting to penetrate the Japanese e-commerce market and other markets in the region, such as Hong Kong. JCB merchant fees are usually charged as a per-transaction commission (percentage).

How can I start accepting JCB?

There are not many JCB Payment Service Providers (PSPs) and Merchant Acquirers (MAs) as for MasterCard and Visa because of the limited popularity of JCB compared to the credit card giants.

E-commerce companies can easily accept JCB credit cards by implementing a payment gateway from a payment service provider that offers global coverage. This lets merchants start accepting payments efficiently and improve the customer experience for a higher conversion rate.