Learn the benefits of network tokenization mechanisms for merchants.

Consumers expect fast and frictionless transactions when shopping online. When merchants fail to meet these expectations – or worse, if a transaction is falsely declined because of the perceived high-risk level – the implications can be significant for businesses.

Although there are many reasons for a transaction to be declined, one of the most common reasons are anti-fraud triggers which can cause a decline due to any number of factors including purchase location, the payment amount, a wrong address, or other criteria that may look falsely suspicious.

Network tokenization, which replaces sensitive customer details with a token that can be used across payment networks, helps reduce the amount of falsely declined transactions by allowing for the payment information behind each token to be automatically updated. This helps to ensure that fewer legitimate payments get falsely ensnared in anti-fraud triggers, while at the same time making it more difficult for actual fraudsters to access customer payment credentials.

How does network tokenization work, what are its main benefits for e-commerce companies, and how can merchants ensure this technology is part of the payment experience they offer customers? Read this article to learn the essentials of network tokenization mechanisms for modern businesses.

Quick recap: What is network tokenization, and how does it work?

7 benefits of network tokenization

How PayU implements network tokenization

Summary: Network tokenization is becoming an industry standard

Tokenization replaces sensitive data with a non-sensitive equivalent: a token. Such a token has no external value – it’s only a reference or identifier mapping back to the sensitive data via a tokenization system. This basic process safely collects sensitive card information and prevents anyone from stealing data.

The tokenization mechanism for cards generates a unique value to replace the customer’s primary account number (PAN). Such a token safely passes through the networks to process the payment without exposing any card details. The card number stays secure within a secure token vault.

Network tokenization helps merchants lower their risk exposure while providing more security for shoppers. With the expansion in the types of online payment methods available to customers, merchants must add an extra layer of security to ensure that the card information is not compromised. Tokenization protects payment data in multiple ways, ensuring that no unauthorized party can reveal the original PAN associated with a generated token.

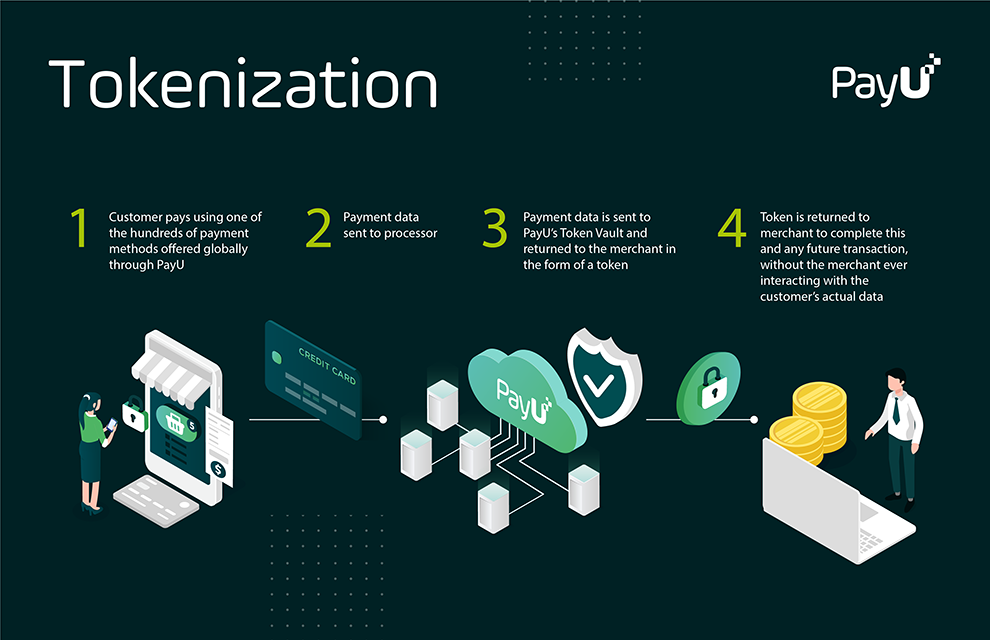

In a tokenized transaction, the merchant never stores or processes the customer’s actual payment details. Instead, when the customer pays for their purchase, all the payment details are sent to the provider’s Token Vault and returned as a token identifying the customer to the merchant. Providers issue tokens in real time. Tokens are then used in predefined environments – for instance, the same card generates one token for use in a specific payment environment and another token for e-commerce transactions.

When a customer buys a product from a merchant, the same token will be used without the business having responsibility over the customer’s data. This is one of the core benefits of network tokenization.

If a merchant wants to store card information in their system without tokenization, they must comply with PCI DSS regulations, which are challenging to implement. Tokenization allows merchants to delegate this responsibility to the payment service provider.

Many payment providers operate Token Vaults, provided they meet the required level of PCI compliance. PayU is Level 1 PCI compliant and uses network tokens to reduce PCI scope and risk for merchants.

Mobile wallets have become an increasingly popular payment method around the world. Tokenization comes in handy here as it allows for secure storage of credit and debit cards in a mobile wallet, which can then be used for online purchases. A mobile wallet uses tokenization to keep its customers’ data secure while giving them the smoothest possible checkout experience.

If you run a recurring payment business, tokenization can also help. It allows merchants to store tokens for each customer instead of their billing information, letting customers continue uninterrupted service while protecting the merchant from being entrusted with a customer’s sensitive information.

One-click checkouts help to retain customers by providing a streamlined checkout experience. Amazon pioneered this form of checkout using tokenization to improve user experiences and retain customers. Around 70% of e-commerce customers abandon their shopping carts – boosting conversions is therefore an essential focus for merchants seeking to optimize e-commerce performance.

One-click checkouts vastly improve customers’ chances of completing the checkout process by removing the obstacles to completing their transactions.

Tokenization allows businesses to store encrypted data on secure servers and reference that data as tokens rather than storing cardholder data directly. This reduces the burden of managing PCI-DSS compliance. Tokenization services also help merchants reduce their compliance requirements by reducing “PCI scope” – the number of components that need to be assessed for PCI-DSS compliance.

Tokenization managed through a third-party provider also offers an extra layer of security for mobile transactions. The additional layer acts as an added biometric check on their identity or requires them to enter a password to access the wallet and move forward through the checkout process.

Since card networks issue the tokens, their issuing banks can update card details automatically. This ensures that all payment cards stored by the merchant are up-to-date, improving the user experience and boosting authorization rates by preventing declines due to reasons like card expiration, loss, or theft.

Users also get to enjoy features such as the ability to use digital wallets or mobile payments where supported.

If the underlying payment account number of the token changes or expires, the token will continue to be valid and can be used to authorize payments. This reduces the number of declined charges due to outdated credentials, increasing authorization rates. Payment providers often combine tokens with payment optimization products to increase authorization rates and optimize checkout conversion.

Tokenization replaces payment card data with a non-sensitive equivalent, significantly reducing the risk of fraud and theft. That’s how it can help decrease declines, chargebacks, and interchange fees. In some instances, it can even shift liability for chargebacks from merchants to issuers.

If your business is affected by a data breach and is found to be holding customer financial data, you could be held legally responsible and open to lawsuits. Tokenization allows storing customer data in a way that keeps it safe for both business and customers.

Payment providers offer network tokenization together with other mechanisms for smoother payment synchronization. For example, thanks to our Level 1 PCI certification, PayU can offer a streamlined and centralized Omni Token solution, which allows merchants to maintain a single card repository that can be used across payment providers without requiring the oversight of sensitive customer data.

Payment tokenization allows merchants to accept recurring payments in their e-commerce business securely. Sensitive card data is transformed into random values that cannot be decoded outside the tokenization systems. That way, merchants can easily store card data for future purchases and accelerate subscription payments for the business and customers.

A data breach has a negative impact on a customer’s trust in a company. Tokenization increases that trust because it ensures that your business does not store the actual financial information directly.

PayU has global agreements for provisioning network tokens from all merchant countries.

The service can be used within the European market to increase approval ratio and customer payment experience where PayU provisions a network token for each saved customer card by the merchant, and then uses the network token for subsequent payments.

PayU’s network tokenization service also complies with initiatives from major credit card companies to process all ‘Card on File’ payments in Europe using network tokens.

In addition, PayU’s global platform also provides more enhanced network token capabilities for merchants who would like to have better management on their provisioned network tokens. This more enhanced service gives merchants the ability to comply with regulations in key markets for processing certain types of transactions only with network tokens.

Where digital transactions have grown in popularity and profitability, the opportunity for fraud has unfortunately followed. To fight the increasing risks, businesses need to introduce proven processes and technologies that reduce the threat cyber criminals pose to payment ecosystems. If payment details are compromised, a transaction is usually declined. The impact of such declines goes beyond individual transactions – costing money and hurting the user experience.

Network tokens reduce risk and improve the customer experience throughout the payments process by reducing exposure to fraud and enabling instant authorization of high-value payments. That’s why PayU collaborates with major card networks and offers merchants the benefit of network tokens generated via our tokenization services.

Network tokens increase approval rates in comparison with payments executed without network tokens, as well as better security and an improved checkout experience. From a compliance perspective, network tokens open the door to managing the network token’s status and suspending it if needed, allowing for easier adoption of EMVCo network token standards with minimal additional integration.