Payment methods have evolved significantly from the traditional ‘cash or card?’ society. To meet the growing e-commerce demand, merchants must keep up with the evolving needs of customers in diverse markets. Perhaps nowhere is this challenge more prominent – and yet more overlooked – than in the question of which online payment methods merchants should offer their customers. In order to deliver a localized checkout experience, many merchants are focused on the question of how to offer as many popular online payment methods as possible – with a need to integrate these as easily and seamlessly as possible within existing payment stacks.

How can merchants determine which payment methods to offer – and what must merchants do to ensure that they can make the most popular payment methods available to customers regardless of geography? Read on for an overview as well as an introduction to PayU’s online payment methods offering.

E-commerce was the long-term trend in retail even before the pandemic, a trend which has only accelerated since everything changed in the Spring of 2020. Shopping online has become the norm for more global customers than ever before – a new reality which has given way to new, alternative, payment methods beyond the traditional credit and debit card providers. Although alternative payment methods are responsible for a growing number of transactions in Western Europe and North America as well, they are particularly prevalent in emerging markets. Credit card penetration in India is just 4%. In Latin America, meanwhile, local payment methods account for more than two-thirds of all online transactions.

Alternative payment methods typically offer customers better flexibility in payments (such as Buy-Now-Pay-Later (BNPL), payment with e-wallets, cash options, and more). At the same time, these online payment methods function can also as a means of digital and financial inclusion for unbanked populations who do not have access to traditional credit cards or bank accounts.

Some alternative payment methods were created as extensions of traditional payment schemes (and thus built atop of already existing infrastructures), while others set up their own unique frameworks separated from the traditional frameworks. From a merchant perspective, this can create a tangling array of financial and technological layers to untangle when it comes to offering payment methods that might not be popular in most of the world – but could be the norm in a particular market.

By accepting a wider range of online payment method options (such as local credit cards, bank accounts, and alternative payment methods) businesses can remain flexible and reach more of the market.

Offering payment methods that are easy and familiar to your new customers is a critical – and often overlooked – aspect of localizing your product for new international markets.

Leverage PayU’s expertise to select the payment methods that will help you reduce friction at checkout, increase payment approval rates, and boost your online sales.

When customers pay for online purchases, businesses should always be mindful of the co-existence of two competing forces at work. On the one hand, e-commerce is becoming increasingly globalized – with credit cards at least somewhat prevalent in most markets around the world. At the same time, we see an exponential growth of local payment preferences, which are often geography-specific and unique to specific target markets.

It is therefore important to build an online payment methods strategy that offers the best of both worlds – encompassing a mix of common and popular global payment method options, while also offering the most important local payment methods in key target markets around the world.

The ability to offer local forms of payment is important for increasing customer satisfaction, reducing cart abandonments, and maximizing transaction approval rates. When expanding into new markets, a willingness to offer local payment method options is an important way that companies can localize their brand and product. In many countries, traditional credit cards and digital wallets are secondary to more popular local payment methods, which are often unique to each market.

In addition to facilitating a higher rate of checkout conversations, transactions using local payment methods often have a higher rate of acceptance since local acquirers and banks are more likely to approve payments from local customers.

The growing number of online payment methods shows the extent to which customers are increasingly open to non-traditional ways of paying. While credit cards are still the most popular payment method in many markets, a growing number of alternative payment methods are offering customers new and often more flexible ways to pay for their purchases.

Let’s dive in and explore some of the most key payment methods in the market today:

The ability to offer local forms of payment is critical for building credibility and trust with online customers – especially when expanding to new markets. In many countries, traditional credit cards and digital wallets such as Apple Pay and PayPal are not commonly used, or are secondary to other more popular payment options, many of which are unique to each market.

From local banks, credit cards, and digital wallets to e-commerce installments and other consumer credit options, alternative payment methods account for a significant share of overall online payment transactions in emerging markets. By using a platform that offers a wide range of local payment methods in multiple markets, merchants selling across borders can offer the payment options most preferred by consumers in each market, with higher conversion and payment acceptance rates, and lower transaction fees.

PayU supports all major credit cards and other common online payment methods used around the world – along with an extensive range of local and alternative payment options that will help you to reach the broadest possible share of customers in any market.

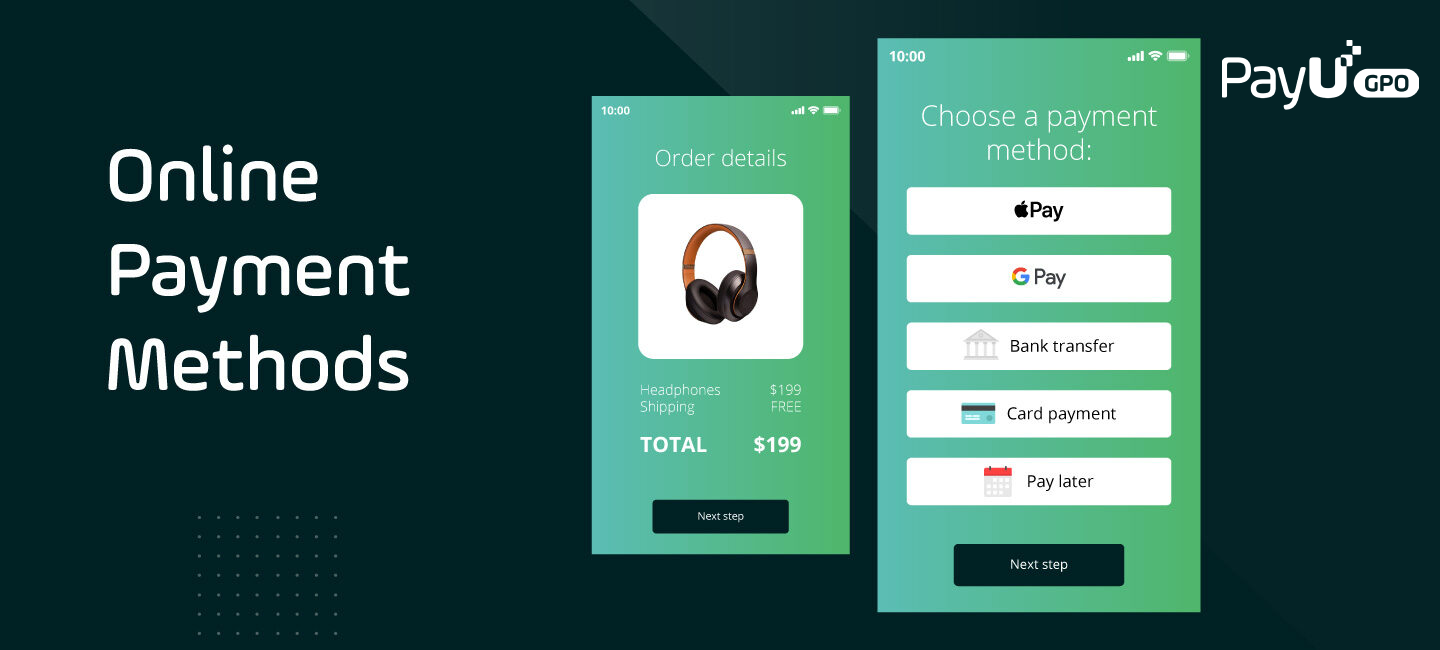

The payment methods in an online transaction refer to the means of payment (e.g. cash, credit or debit card, bank transfer, or alternative payment methods). PayU’s platform provides access to hundreds of local and global online payment methods around the world, helping merchants to maximize their reach.

Although credit and debit cards remain the most popular online payment methods globally, this varies greatly by region. Digital wallets, Buy Now Pay Later (BNPL), and other alternative payment methods are increasing in popularity around the world. In Europe, many online orders are paid via direct bank transfer. And in many emerging markets, cash voucher schemes account for a significant share of e-commerce transactions.

The most popular payment method is different in every country. Even in countries where credit and debit cards are the most popular online payment method, the market is often dominated by cards issued through local banks as opposed to the major credit card companies. In order to reach the most customers, merchants should seek to offer many different local and global online payment methods to meet a broad range of needs.

Offering more online payment methods helps merchants meet customers where they are, resulting in a better checkout experience, fewer shopping cart abandonments, and more repeat customers. Offering local payment methods also helps to increase transaction approval rates, leading to increased revenue and fewer false declines.

The ease of integrating local payment methods depends on the capabilities of the payment gateway. Many payment gateway technologies only provide access to a limited range of payment methods. By connecting to PayU’s global platform, merchants can offer hundreds of popular local payment methods and accept payments in any global market.

We are constantly updating the payment methods available locally and globally through PayU. To learn more about all of the different payment methods supported by PayU, browse through our payment methods catalog.