Merchants can increase payment approval rates using automated card updating, advanced payment analytics, smart routing, instant retry, 3DS consolidation, and network tokenization.

All that you need to know about approval rates.

While online shopping offers numerous conveniences, the checkout process often isn’t one of them. Online shoppers face a higher likelihood of their transactions being declined. Merchants who don’t address this issue risk permanently losing customers, damaging their reputation, and negatively impacting their business’s overall health.

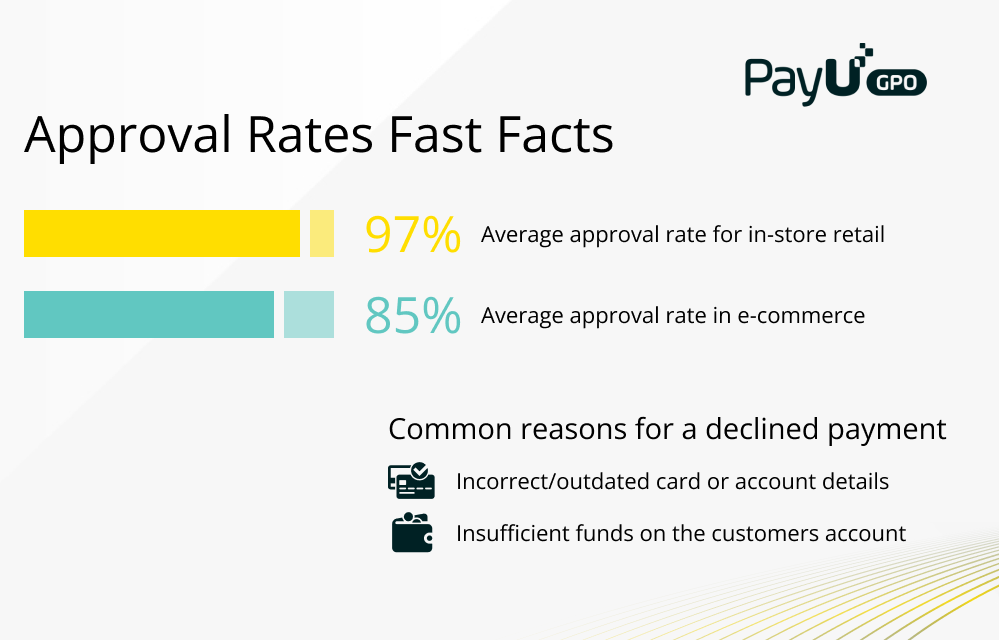

In-store transaction approval rates are close to 97%, whereas e-commerce transactions see an average approval rate of around 85%. This difference, though seemingly minor, results in poor checkout experiences, customer frustration, and significant revenue losses when considered across hundreds or thousands of transactions.

Why is optimizing payment approval rates crucial? And how can merchants boost the success rate of online payments?

Here’s a detailed guide to understanding approval rates, along with proven strategies for improving them.

What is the payment approval rate – and why does it matter?

6 strategies to boost approval rates through payment optimization

Summary: Maximize e-commerce success by optimizing approval rates

The payment approval rate is the result of dividing the number of approved transactions by the number of attempted transactions over a fixed time period. It’s a rate that shows the extent to which payments started by customers get approved in your online store.

Why does the approval rate matter? Because it tells merchants how much money they may be losing due to declined transactions. Declined transactions have consequences that extend beyond just immediate revenue loss. According to some estimates, only 25% of customers will attempt to use another card when their transaction is declined, while 39% will abandon their cart entirely.

Stagnant or declining sales can have many causes – some of which businesses can trace and remedy to improve sales figures. One such “fixable” cause is addressing payment declines and boosting approval rates.

Even the most successful online stores might be leaving thousands of dollars worth of revenue on the table due to approval rates that are lower than they need to be.

Soft declines

A “soft” decline occurs when the issuing bank approves the transaction, but the transaction fails anyway. The most common reason for a soft decline is insufficient funds available in an account to make the purchase.

Other reasons behind a soft decline might include:

The last two reasons are ambiguous since there is not always a clear explanation from either the consumer or the merchant.

Hard decline

A “hard” decline occurs when an issuer denies a transaction because of limits set by the issuer, even if sufficient funds are available in the consumer’s account to complete the transaction.

To improve approval rates, it is helpful to understand the most common reasons why payments are declined.

Here are a few issues merchants struggle with when it comes to payment declines:

Although each of the following reasons is legitimate to decline a card payment, poor communication, misalignment, and ambiguity between all entities involved in a payment transaction often lead to declined transactions that could have been approved.

Understanding these issues and taking the appropriate steps to remedy them is how merchants can drive higher payment approval rates.

Merchants can boost revenue from recurring payments by using automatic card updating and recycling services. Payment processors usually offer a service that allows merchants to submit transactions using the original account information obtained from the cardholder while ensuring that the current information is used for the authorization.

Not only is this useful for recurring or subscription billing, it also applies to merchants who can reduce friction in their consumers’ experience by storing their payment information for use in subsequent purchases.

Another way to improve approval rates is by using data-informed services such as advanced payment analytics.

With a unified analytics dashboard, merchants can get their hands on a single, real-time view for all global payments data.

While data in itself won’t guarantee higher approval rates, improving the quality and usability of payment data can help show merchants which payment optimizations they should implement in order to drive higher payment acceptance rates.

A simple and straightforward analytics panel allows you to create pre-configured as well as custom reports based on business needs, making reporting easier and more powerful than ever before.

Whether it’s building cross-provider reports, comparing provider performance, or segmenting transactions by business unit, an advanced analytics dashboard helps merchants leverage insights to optimize payments anywhere in the world.

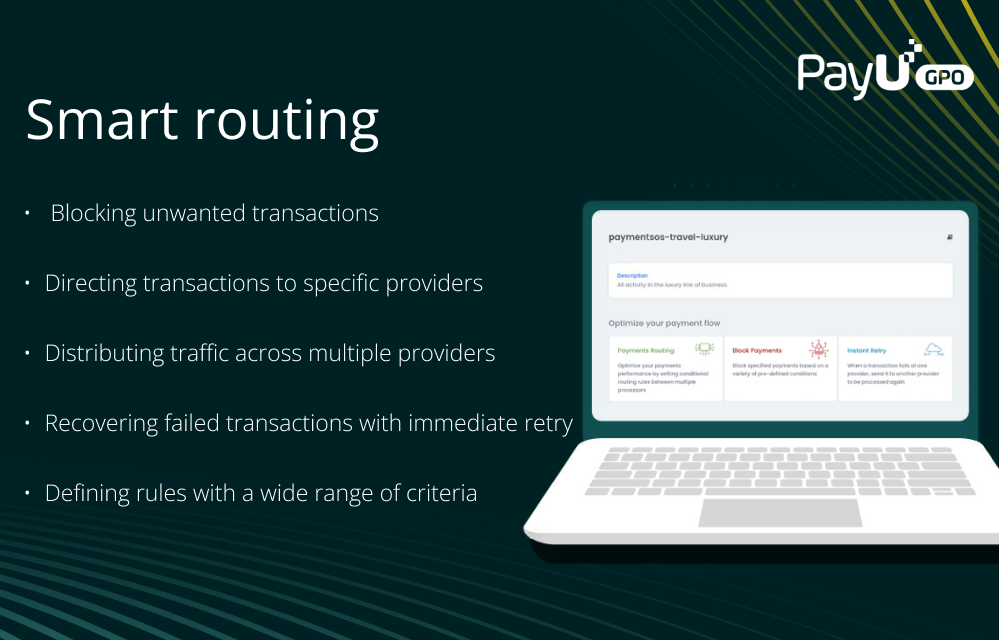

A payment gateway is the central nervous system of the payments world, directing transactions to acquirers and payment service providers for processing. The payment gateway affects everything – from scalability and client experience to payment approval rates.

That’s why intelligent routing capabilities are essential for optimizing payment traffic and improving approval rates.

The PayU orchestration platform provides a US-patented Smart Routing Enginethat offers plenty of smart routing configurations to support any business goals. Merchants can choose their preferred routing configuration – optimizing for lower fees, higher approval rates, or other custom criteria. Routing rules can be based on a variety of factors, including the issuer, geographical area, transaction size, and more.

When choosing a payment gateway, merchants should look for a solution with dynamic routing capabilities, allowing businesses to create a more efficient payment infrastructure that can scale and adapt to market changes.

Another helpful element when seeking to boost payment approval rates is a good Instant Retry tool, which can automatically re-route failed payments to a merchant’s bank account.

PayU’s Instant Retry feature is a unique capability that is used to save failed transactions by retrying them through pre-configured routing rules. Using the PayU Decision Engine for easy setup, merchants can manually define retry criteria according to specific error codes, card country, or other factors.

With Instant Retry, e-commerce businesses can increase payment approval rates and recover payments that would otherwise be lost due to both hard as well as soft declines.

The 3D Secure 2.0 payment protocol was developed in response to the European Union’s Secure Customer Authorization (SCA) requirement, which was implemented in 2019 and is designed to ensure more secure online payments while protecting consumers against fraud.

But while 3DS 2.0 can bring a number of benefits to merchants, it can also result in lower approval rates in locations outside the EU with less stringent anti-fraud regulations.

Given the variation in the regulatory landscape, a good payment processor can help merchants maintain optimal approval rates by tailoring the 3DS strategy and constantly engaging with merchants and banks. Smart Routing tools, for example, can help merchants route payments through the optimal 3DS protocol (3DS 1 or 3DS 2) based on processing location.

Many modern solutions use merchant fraud data to develop a 3DS exceptions strategy. This includes transaction monitoring as well as dedicated merchant reports to ensure optimal approval rates during the 3DS adoption stage.

Merchants should also make sure that their payment processor maintains close relations with banks in order to ensure optimal acceptance of 3DS exceptions.

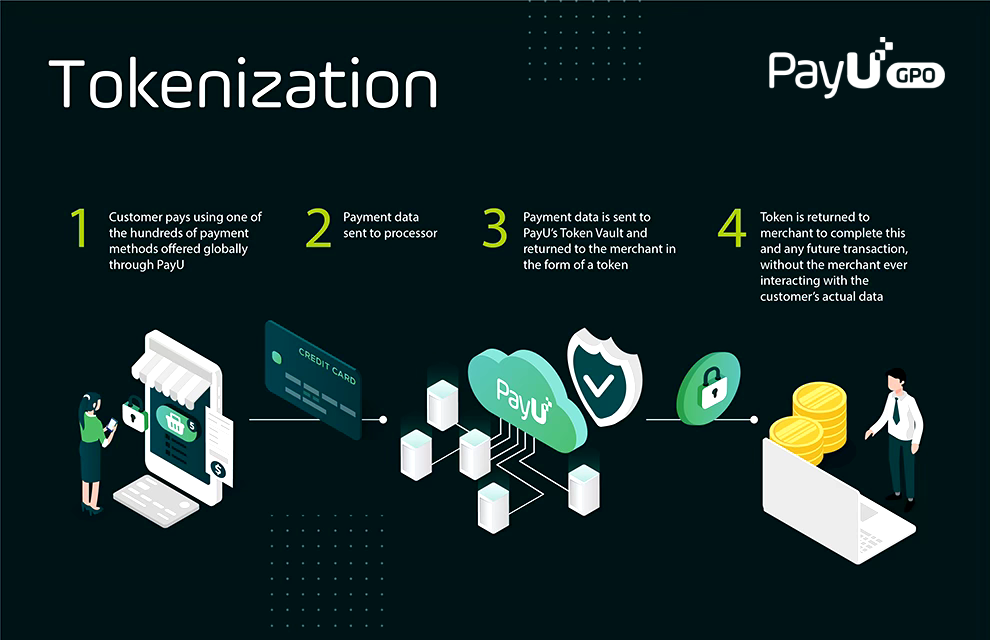

A final way that merchants can increase their approval rates is by using network tokens to authorize payment transactions.

How does network tokenization work? When a customer enters their card details, they are immediately replaced with a card network token. The token is unique for both the merchant and their customers. When a customer makes a payment, the payment system transmits the token into card details.

What if the customer’s card details have changed? The system will map the new details with the token. This allows merchants to achieve higher approval rates and capture higher transaction volume by avoiding lost and/or expired card declines.

Naturally, network tokenization also leads to fewer false declines as tokens provide more information and greater visibility to card issuers during payment authorization, helping to build a more secure and frictionless transaction flow.

Online payment declines have risen for many e-commerce segments, and many merchants face mounting issues related to dropping approval rates. Understanding the possible reasons for declines is the first step, but tracking and optimizing them constantly is a challenging task.

As e-commerce business expands, merchants may have little time to optimize payments independently. Thankfully, merchants can solve this dilemma through their choice of payment solution.

A quality payment gateway that achieves the right balance for payment success and efficiency can help streamline and generate action items to combat low approval rates – resulting in higher sales and more satisfied online customers.

Merchants can increase payment approval rates using automated card updating, advanced payment analytics, smart routing, instant retry, 3DS consolidation, and network tokenization.

Optimizing payment approval rates is crucial because it can significantly impact online businesses’ checkout experience, customer satisfaction, and revenue losses.

The payment approval rate is the percentage of approved transactions out of the total attempted transactions over a fixed period. It matters because it shows merchants how much revenue they may lose due to declined transactions.

The two types of payment declines are soft declines, which occur when the transaction fails even though the issuing bank approves it, and hard declines, which occur when an issuer denies a transaction due to limits set by the issuer, even if sufficient funds are available in the consumer’s account.

Factors that lead to payment declines include incorrect or outdated card or account information, insufficient funds on the customer’s account, network unavailability, unspecified “Do not honor” declines from the issuing bank, and mistakes in the merchant’s or card network’s fraud and risk mitigation tools.

Payment optimization can increase e-commerce success by streamlining the payment process, reducing friction in the customer experience, and providing actionable insights to combat low approval rates, resulting in higher sales and more satisfied online customers.