A good payment platform should help merchants fight fraud and stay on top of payment security requirements – while keeping the checkout experience frictionless and safe.

Securing e-commerce applications has become a top priority for online businesses. That’s because fraud can cost a lot.

On one side there is the potential for loss of reputation and customer trust. On the other, there is the sheer cost of fraudulent transactions. Global payment fraud grew by 3 times between 2011 and 2020, reaching $32.39 billion in 2020. Payment fraud will generate $40.62 billion of expenses by 2027 – a further 25% increase.

Which payment security tools can help merchants ensure a seamless flow of payments while fighting fraud efficiently?

Here is an overview of the most essential payment security practices e-commerce companies should be looking for when choosing an online payment provider.

Why is Payment Security Important?

Payment Security Essentials for Online Merchants

A transparent approach to payment security goes a long way when creating a lasting relationship with customers. Trust is everything in e-commerce – so while cutting corners when it comes to payment security might be a clever way to superficially lower costs in the short term, it is bound to come back to bite merchants down the road.

Proper payment security has the power to make or break a merchant’s business. You could spend years establishing yourself as a trustworthy brand and then lose it overnight because of a data breach or chronic fraud.

This is the business case for payment security – in addition to being the right thing to do, insecure payments are a major risk that should not be taken lightly.

There is also a regulatory and compliance component. When accepting payments, merchants need to meet important requirements – especially if they’re selling internationally. If merchants fail to do so and customer information is compromised, the penalties to the business go beyond loss of reputation and can include massive fines from industry and government regulators.

The need to fight fraud and maintain consumer trust online is a big part of why the payment industry has set up guidelines for handling payments around the world. The European Union, Payment Card Industry Data Security Standard (PCI DSS), and the International Standards Organization all have important online payments rules that shape the payment industry. Merchants need to follow all of these rules in order to protect customers while staying out of trouble.

Fortunately, a quality payment provider can make it easy for merchants to stay compliant with industry standards while processing payments with a high level of security.

Here are some of the key payment security features that merchants should be looking out for when searching for the right online payment solution.

PCI DSS is a global security standard for accepting and processing credit cards. Launched in 2006 by an alliance of major credit card companies, the standard includes 12 key requirements as well as more than 400 sub-requirements and test procedures.

To be PCI compliant, merchants must meet a number of requirements and continually identify, document, and (if necessary) remediate business-level systems and processes that handle user credit card data.

Every entity that either processes, stores, or transmits cardholder data must be compliant with PCI DS. Fines for businesses that fail to comply can be crippling. For large companies, fines may reach well over $100,000 per month.

Some consider PCI compliance too expensive and time-consuming, but many payment providers make PCI compliance easier for merchants. PayU offers a variety of ways to reduce PCI scope, limit responsibility and risk, and remain compliant.

One of the best options for limiting PCI scope is tokenization (keep reading below), which replaces customer payment data with a “token” so that even the merchant can’t see the original data. This reduces PCI scope by making the payment provider responsible for safeguarding the payment data.

By using this solution, businesses can save on compliance costs while at the same time offering customers a more secure payments experience.

Tokenization is a mechanism that protects user card information by generating a unique token for each transaction. In essence, it prevents merchants from collecting sensitive data.

For example, if a customer buys something from an online store, the application won’t receive their credit card information. Instead, it will receive a unique code identifying the customer as the buyer. The next time they visit that merchant’s site to make another purchase, the solution will use the same code.

Many third-party payment processors use tokenization as long as they’re PCI DSS compliant. As a PCI Level 1 Certified Payment Processor, PayU can offer merchants a single, cross-platform tokenization solution with a centralized token vault. The token vault allows for synchronization between all of the merchant’s payment providers and payment methods, reducing the need to coordinate between token systems (which can be an issue for merchants with a more complicated payment portfolio).

By collaborating with major card companies, payment processors can offer merchants the benefit of network tokens. Network tokens come about via tokenization services offered by card networks. What differentiates network tokens is that they also allow payment processing without ever exposing the shopper’s actual card details.

And here’s the best part: in addition to better security and an improved checkout experience, network tokens offer higher approval rates in comparison with payments executed without them. It’s a win-win solution – good for security as well as performance.

Digital identity is a way of verifying a user’s identity on the internet. From online purchases to self-service onboarding activities and multiple accounts or money-based actions, digital identity verification prevents fraud and protects sensitive digital activities.

When working with a payment provider, merchants should ensure that the digital identity measures that the payment provider implements don’t impact the customer experience in a negative way – for example, by prolonging transaction time or adding inconvenient steps for the user.

To provide high quality digital identity verification that doesn’t interfere with transaction speed and efficiency, payment providers like PayU often team up with digital identity verification companies.

PayU has developed a partnership for this purpose with AU10TIX, which harnesses advanced AI solutions to provide shoppers with the fastest and safest digital identity verification available.

As more and more business moves online, cybercrime isn’t going away any time soon. The situation is in fact quite the opposite – cybercriminals are perpetually probing for weaknesses in payment systems while developing new and more sophisticated forms of attack. Merchants need to be on higher alert today than ever before.

Payment providers know the risks of cybercrime and the good ones are aware that security is now a more essential value proposition when it comes to payments than ever before. To protect merchants and consumers and deliver the most secure online payments, PayU offers an anti-fraud module that can be provided either out-of-the-box on our own platform or as a standalone module integrated with other payment systems.

PayU’s solutions identify, monitor, and prevent potential threats by monitoring customer and third-party data across 190 countries. By combining our own solutions with those provided by Feedzai and other trusted third parties, we are able to process over 10 million transactions each day while keeping customers safe.

As part of the European Union’s Payment Security Directive 2 (PSD2) regulations, Strong Customer Authentication (SCA) is now mandatory for all online transactions in Europe.

To reduce the risk of fraud, the requirements for SCA apply whenever an EU-based shopper makes a payment. While there are some exemptions, merchants shouldn’t rely on them when it comes to accepting online payments in Europe. This is because in addition to the risks of non-compliance from a regulatory point-of-view, implementing SCA standards can help merchants to boost approval rates and ensure more successful online payments everywhere in the world.

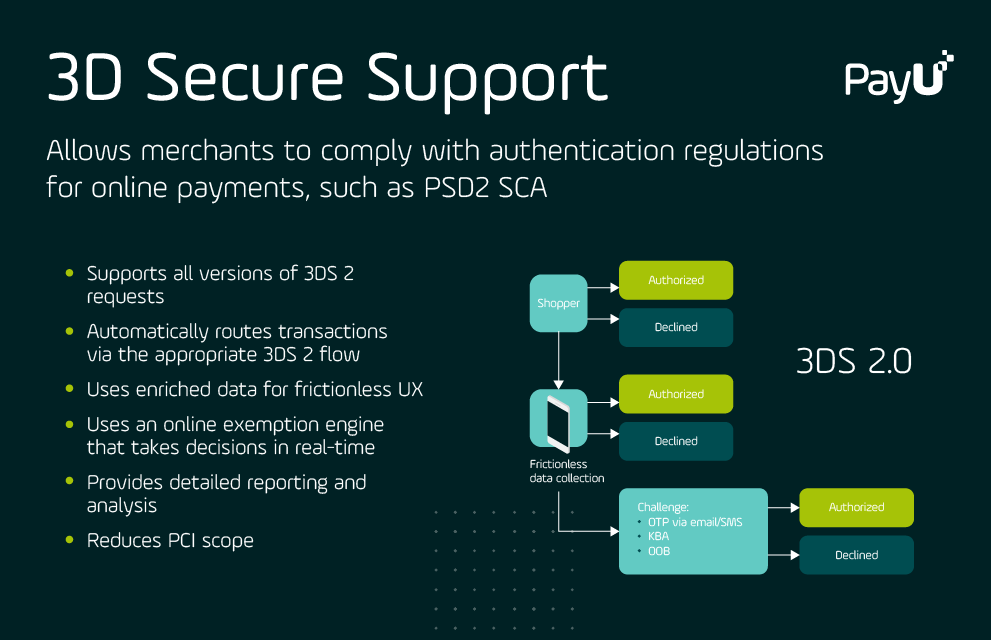

One mechanism for adhering to PSD2 is the EMVCo 3D Secure payment protocol (also known as 3DS 2), which is designed to help merchants comply with SCA rules while providing a better user experience at checkout. 3DS 2 are improvements to the original 3D Secure protocol for verifying digital payments. In addition to compliance, 3DS 2 makes collecting and processing customer payment information easier.

Merchants can streamline SCA implementation and access the other benefits of 3DS 2 by working with a payment provider that manages 3DS requirements as part of the overall product offering.

With 3DS 2 on its way to becoming a global standard, but not quite there yet, PayU supports merchants with 3DS implementation while at the same time mitigating the complexity and variations across different regulatory locations. For example, merchants can use the Smart Routing Engine to configure transactions according to which 3DS protocol (3DS 1 or 3DS 2) delivers higher approval rates in a given region.

PayU’s anti-fraud module also supports 3DS by authenticating transactions according to local regulations and routing payments via the appropriate local 3DS flow.

Frictionless transactions don’t have to be at odds with ensuring a high level of security.

At PayU, we empower businesses with solutions that maintain the highest payment security standards while offering great experiences to their customers and simplifying the essentials of industry and regulatory compliance.

In addition to developing our own solutions, we have partnered with industry-leading security companies to steadily improve our product offering while operating a payment platform that allows merchants to accept seamless and secure online payments from any market in the world.