See why embedded finance represents the future of payments and financial services – and how you can implement embedded finance solutions in your business.

It’s no secret that the outbreak of COVID-19 in 2020 saw a massive increase in the number of businesses accelerating their digital transformation. Companies across all industries rushed to upgrade outdated systems and replace legacy technologies with cloud-based software designed to improve communication and accessibility with clients.

As the world slowly enters a “new normal” more than two years after the start of the global crisis, the longer-term impacts of the investments made over the course of 2020 and 2021 are slowly coming into focus.

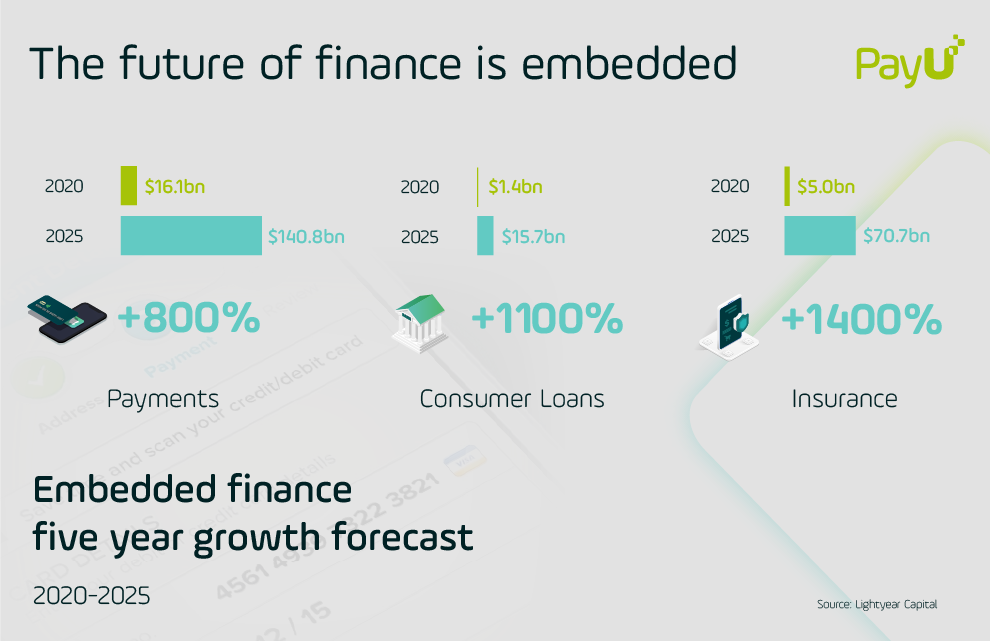

Within payments and fintech, one of the key industry trends to watch is the rise of embedded finance, which is playing a bigger and bigger role in many aspects of financial services. LightYear Capital estimates that embedded finance services will be worth almost $230 billion by 2025 – a tenfold increase over 2020 (when it was already worth $22.5 billion).

What’s next for embedded finance? And which factors will be driving this key technology trend? Keep reading below to learn more about embedded finance, some examples of the primary use cases, and how your business can benefit.

How Does Embedded Finance Work?

Four Trends Driving the Future of Embedded Finance

Getting Started with Embedded Finance

Summary: The Role of the Payment Provider in Embedded Finance

Embedded finance generally refers to the inclusion of financial or banking services in non-financial company.

The additional services benefit customers by offering a one-stop shop for their needs, while companies benefit from customer retention and new revenue streams. Whether payments, lending, insurance, or investing, core financial services are increasingly being embedded into native applications as an additional service to improve the customer experience.

A few years ago, providing such services required a massive investment in resources, time, and technical development. But integrations are now easier than ever before thanks to the impact of regulatory change (like PSD2 in Europe, which helped open the door to open banking); improving technology (easier API integrations that enable non-finance companies to connect to financial services); and the consumer and industry norms that are both shaping and being shaped by both.

Both companies and consumers benefit from a more seamless experience that makes doing business online easier than ever before.

As the financial industry shifts to accommodate new technologies, it opens itself up to many exciting opportunities. For example, a popular ride-sharing app has created prepaid cards for its drivers, offering instant payments while also significantly reducing driver fees – all of which help strengthen customer loyalty.

In addition, many non-bank organizations have access to even more data points about their customers’ financial needs and behaviors because of open banking and the PSD2 directive. These entities can often provide better recommendations around financial products than their banks, leading to increased sales opportunities for the company at the point of need.

Even more exciting is that these new technologies allow companies to expand into additional profitable areas quickly. The company Square started as a payments processor but has since evolved into a point-of-sale company, CRM solution provider, and inventory management service – introducing multiple revenue streams which have allowed the company to grow.

From the supply side, offering financial services gives companies increased ownership of the total customer experience, with more holistic insights on customer behaviors and patterns that, in turn, help them identify and serve new customer needs that aren’t currently catered for by existing products and services.

On the consumer side, embedded finance helps to streamline common financial processes, making it easier to access services and purchase products.

In the past, individuals had to go through the bank’s process to access credit or through a separate payment interface to purchase something online. Now, with embedded finance, consumers can make a purchase and get credit from one place: the point of service.

We already see examples of cashless and cardless payments via mobile wallets and QR codes in the payment space.

Banks are now redefining their roles as facilitators of payments. Some retail stores have eliminated payment terminals altogether in favor of biometric-based payment systems that identify users through thumbprints, iris scans, and voice recognition. And car companies are working with payment networks to create connected mobility experiences that enable users to purchase fuel and toll roads, as well as schedule vehicle maintenance and parking fees through voice commands embedded in their vehicles.

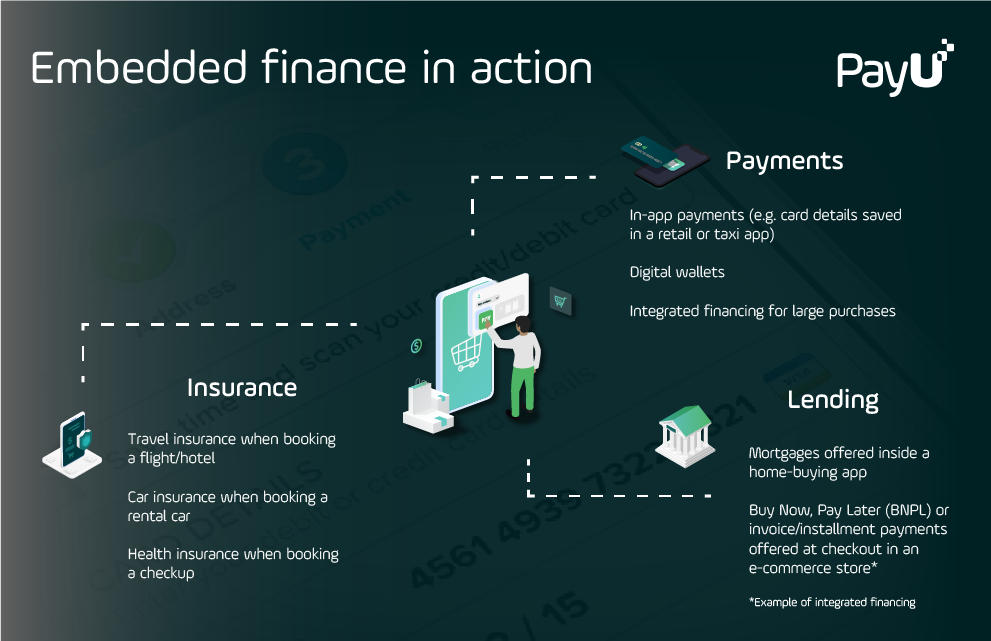

Some other everyday examples of embedded finance include:

Here are some further examples of where the embedded finance trend is going:

Embedded payments are the most popular examples of embedded finance, enabling businesses to integrate payments into their products. Businesses across practically every industry can easily add new payment methods to streamline the checkout experience for users while controlling the experience from start to finish.

The trend of buying now and paying later, known as BNPL, has reached both online and point of sale (POS) to create new lines of credit for modern shoppers.

BNPL empowers consumers to shop differently, whether investing in a higher-quality piece of home technology or a new desktop computer.

Evolving from BNPL, integrated financing takes the trend one step further. Businesses like hotels and car dealerships have started embedding sophisticated financial tools that can incorporate further information on creditworthiness, such as data on the customer’s credit score and credit history, in order to provide more financial flexibility to consumers by offering credit for large purchases at the point of transaction.

Embedded investment enables businesses to offer their customers access to funds and stocks. The most basic use case allows companies to integrate stock market investing capabilities into their product offerings. API-based brokerage firms are leading this trend by offering APIs to manage end-to-end flows including opening of accounts, funding, trading, management, and market data.

Many businesses now offer insurance for customers purchasing a new product or service. Businesses can embed the insurance financing tools in products and services to help deliver Integrated Finance & Insurance Services (IFIS) in just minutes. This helps businesses grow sales and increase loyalty by delivering insurance solutions that work in real time.

Underlying embedded finance and Banking-as-a-Service (BaaS) is a change in consumer habits. More and more customers are increasingly open to contracting financial services with alternative providers to banks.

In Germany, 61% of respondents of a recent survey were willing to use financial services from the e-commerce brands analyzed in the study.

According to another report, 46% of millennials say they would consider opening a checking account with Amazon if it came with benefits such as identity theft protection, roadside assistance, travel insurance, or product discounts. More than 30% would be willing to do the same with companies like Starbucks, Uber, Facebook, or Google.

This new trend in customer behavior makes embedded finance a field of incredible growth potential – not only for e-commerce but in other areas such as wealth management or insurance.

New technology capabilities such as APIs open the door to easier integration of banking services into any online retail store. Banks can scale their BaaS offerings using automation solutions and APIs and place embedded finance within reach for more companies.

At the same time, online retailers and other businesses can embed financial services into their digital experiences thanks to modules built by others. In doing so, payments, lending, deposit, and checking accounts become yet another product capability that enriches the customer experience.

Companies can embed payments directly into their products. This trend is now expanding to other businesses thanks to innovations offered by payment processors.

By embedding payments, merchants allow their customers to have one cohesive experience between all aspects of their platforms. This often gives them more control over the payments process from start to finish.

This Bank-as-a-Service model grew by $22.5 billion in 2020, which experts predict will represent only the tip of the iceberg for embedded finance in the coming years.

Regulatory trends such as PSD2 and open banking foster the development of banking APIs and universal access to services. Since banks now have to comply with these novel requirements, which often involve IT modernization, they often consider expanded or new BaaS business models to recoup the expenses which such projects generate.

Moreover, customer expectations for data and account information portability are changing. This only adds momentum to the accelerating IT modernization and BaaS projects.

As a result, banks are actively looking for new revenue models and alternative sources of product growth.

An initial step toward designing an embedded financial strategy is the analysis of digital finance goals and decision-making regarding the tools to embed. The objectives may be improving customer service, expanding an existing customer base, or launching a new venture to meet a specific audience or market need.

For example, if you seek to improve customer service and satisfaction, an embedded payment could be one method to explore. A BNPL model could make products or services more accessible to certain customers. Embedding other financial services, meanwhile, can make it easier for your business to offer a one-stop-shop concept. But in order to pick the right solution, businesses first need to envision the best use case.

Embedding financial services by a non-financial business can be done independently or by partnering with service providers who act as key enablers of this technology.

Selecting the right partner with experience helping companies to deliver embedded finance solutions can help shorten the journey from concept to implementation.

As a provider of global payment solutions and fintech focused on high-growth emerging markets, PayU works with companies seeking to embed payments and other financial services directly into key business applications.

Here are some key features to look for when it comes to embedding payments into your company’s interface with customers:

The pandemic has been a massive accelerator for digital transformation across a number of industries. Thanks to a combination of new technology, easy API integrations, and regulatory changes, embedded finance solutions are playing an ever-expanding role in the e-commerce and digital services landscape.

Consumers are now seeing the impacts of embedded finance in everyday applications – with this comes the growing expectation that everything from payments to everyday credit and insurance options can be accessed at the convenience of a click or phone tap.

As embedded finance continues to grow, merchants must be prepared to offer the most convenient possible interface to their customers, while keeping up with industry trends and maintaining appropriate cybersecurity precautions.

To integrate embedded finance and do it well, businesses should ensure their payment solutions provider has the right experience and platform to help embedded finance functionalities – while keeping the user experience both frictionless and secure.