BNPL is the talk of e-commerce. See what’s behind the rise of this important online payment method, and how can merchants make the most of it.

Today’s online shoppers look for convenient online payment method options that make the payment process quick, smooth, and familiar. To meet these customer expectations, one of the key trends in the online payments space is the simplification of payment and checkout processes.

In order to meet this need, Buy Now Pay Later (BNPL) payment options are becoming increasingly prevalent, simplifying consumer decision-making while allowing merchants to reach a new swath of customers. BNPL payment methods translate into tangible benefits to merchants: more customers, higher basket values, and fewer abandoned carts.

The volume of global sales processed through BNPL reached $93 billion in 2020, a number which is expected to rise to more than $181 billion by the end of 2022, growing more than 40% per year.

As an alternative source of credit, one e-commerce demographic that BNPL helps merchants to reach are younger consumers, who often have a limited credit history and low credit scores. No wonder: one-third of Millennials and almost half of Gen Zers don’t have a credit card. This growing population of thin-file customers presents an opportunity for alternative lenders in the BNPL space – as well as a challenge, given the lack of credit history that traditionally helped determine risk at account opening.

Which customer behaviors and industry trends are driving the rise of BNPL payment methods – and why should merchants be sure to add it to their checkout formula?

Read on to find out more.

Benefits of BNPL for customers

Research shows that different factors drive consumers to use BNPL versus credit cards. Transparency of fees, spending monitoring, and ease of use are some of the main reasons why so many consumers are turning to BNPL solutions.

A credit card may be easier to access when it’s available directly in the customer’s digital wallet. However, the flexibility and reliability of BNPL’s installment structure gives consumers greater peace of mind as they feel more in control of their spending.

Emerging markets such as India, Mexico, and Indonesia stand out in terms of consumer adoption, with over 50% of consumers having used BNPL to fund transactions.

Adoption is also high in countries like Belgium and the Netherlands. The same is true for the Nordics, which – together with Germany – are at the top in terms of BNPL’s share of total e-commerce transactions globally.

Get an overview of BNPL solutions around the world in our BNPL guide from earlier this year: 22 Global Leaders in Buy Now, Pay Later.

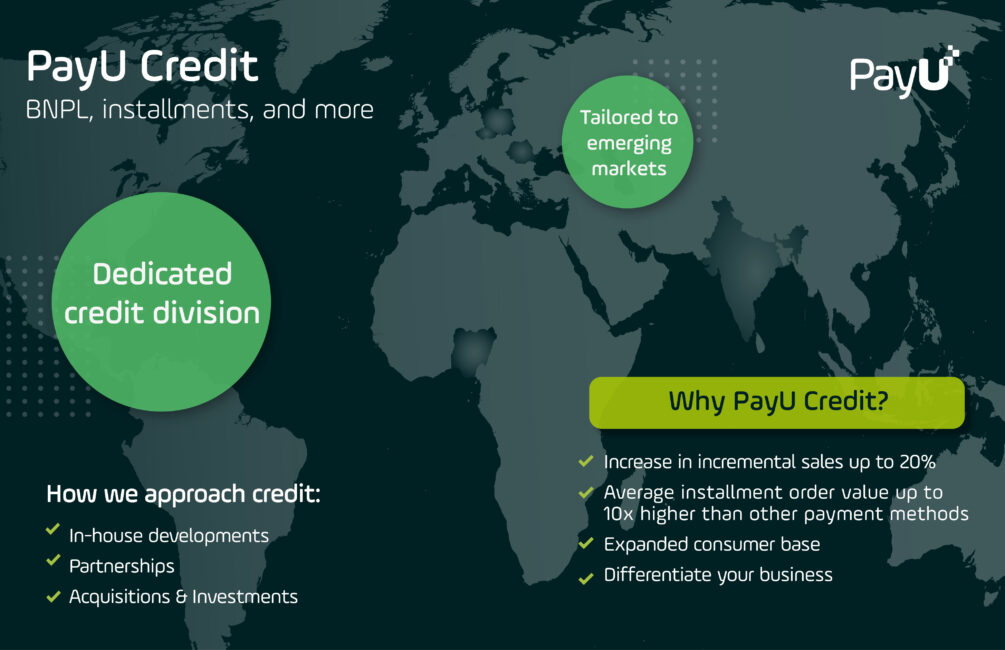

Within the fashion vertical, many shoppers are interested in flexible and convenient forms of online payments such as BNPL and installment-based payments.Installment payments in fashion – one of the most popular payment methods in many emerging markets – can help merchants reach more customers while achieving incremental sales increases from 20% to 30%.

Other key verticals include electronics, furniture and home goods, sports, and home fitness equipment, and travel. In the US, for example, recent studies indicate that buying electronics is the most common use of BNPL, with nearly half (48%) of BNPL users saying they’ve used it for this reason.

Credit is a mechanism customers use most often to finance larger purchases. The same holds true for BNPL. When consumers were asked how much they had spent on their most recent BNPL purchase, the average amount was $689, according to a recent study. The same group of US respondents reported that their average outstanding amount owed from BNPL purchases was $883.

During the checkout process, customers only need to add their details once. The second and subsequent purchases don’t require users to complete any more payment steps. This type of one-click payment is very easy to use and particularly efficient on mobile devices, opening the door to more streamlined e-commerce.

Customers benefit from delayed payments with BNPL. This enables them not only to pay after several weeks but also – in the case of fashion and apparel – to try on the ordered items and return them to the merchant in case they don’t fit without spending any of their money. In doing so, BNPL makes it easier to settle returns, adding a layer of convenience while also building trust in online purchases.

Another powerful benefit of BNPL is the role it plays in financial inclusion. Having a credit history and access to credit cards is only possible for individuals who have access to banking services. BNPL can grant credit to unbanked consumers or one who may be denied traditional credit forms, making an impact on large population segments across the world, especially in China and India, which have the largest unbanked populations (225 million adults in China and 190 million in India), as well as Latin America.

BNPL comes with many unique benefits for merchants. Through BNPL and other credit products, merchants benefit from a larger customer base, increased online sales, and higher average order values compared to traditional payment methods.

In addition to boosting the accessibility of e-commerce, BNPL also increases buying power. Consumers spend 55% more when they can split the payment into installments. This is corroborated by data from the PayU platform, which shows that BNPL products increase the average e-commerce order value substantially – up to 10 times more than for other online payment methods.

Moreover, installment payments in specific verticals such as fashion can help merchants achieve incremental sales increases of 20-30%.

The availability of BNPL as a payment method helps increases the conversion rate by offering a wider and more convenient variety of payment options. Merchants who have implemented it report fewer abandoned shopping carts at checkout, which also drives increases in incremental sales and revenue.

One survey showed that 32% of consumers aged 18-39 made purchases they would’ve otherwise postponed if they saw the option to pay via BNPL.

But that’s not everything. Merchants who implement BNPL also see a higher volume of repeat sales. A total of 28% of customers are more likely to shop with a merchant again if it offers a BNPL option.

By letting customers spread payments over a defined period of time, BNPL is meeting the market need for an alternative to traditional credit card payments. In addition to facilitating a smoother checkout experience in many cases, BNPL helps to make e-commerce more inclusive for populations without access to conventional finance.

One report noted that in Asia, merchants stand to onboard 1 billion underbanked people as new customers if they implement BNPL solutions capable of accurately predicting the credit risk of those consumers.

BNPL solutions may have exploded during Covid-19, but they’re more than just a pandemic trend. The global BNPL market value is currently projected to reach $656.3 billion by 2026.

In the future, more and more customers will turn to BNPL solutions on their mobile devices in particular. Mobile BNPL is projected to grow faster than conventional BNPL between now and the middle of the decade, registering a 27% CAGR between 2020 and 2025 (compared to the 10% CAGR of the overall e-commerce market).

Another powerful trend shaping BNPL is consolidation across the market, driven by further investments in the field and cross-industry partnerships. According to McKinsey, fintech companies currently hold the majority of BNPL market share, having already captured about $8-10 billion in annual consumer financing revenue. However, banks are actively moving into the space, and many of them are ready to take the BNPL scene by storm.

The expansion of BNPL is also likely to dovetail with another big trend in payments – the emergence of the Super App. Already highly common in Asia, where platforms such as Alipay and WeChat Pay enable consumers to access a wide range of products, services, and features, Super App features are likely to become more prevalent in the coming years in other parts of the world, as well.

As part of this trend, BNPL providers with strong brands may well seek to expand their app capabilities to include services beyond payments.

PayU has been at the forefront of the BNPL trend in a variety of markets, offering a range of BNPL payment options via PayU Credit – including installment payments, credit card installments, and credit or cash loans in selected markets – depending on the local market’s requirements and the popularity of the payment method among consumers. Our offer is diversified and relies on both partnerships and direct offerings.

Representing a combined consumer population of nearly 60 million people, Poland, Romania, and the Czech Republic are three of Europe’s most compelling growth markets for e-commerce. With offices in all three countries, PayU is deeply rooted in the Central and Eastern European region.

PayU Credit is the biggest online credit broker and distribution platform on the Polish e-commerce scene, facilitating nearly $1 billion in credit volumes processed and over 2,500 merchants using PayU Credit solutions. We’ve partnered with a network of leading consumer finance and BNPL providers to create multiple consumer credit options through a single API.

In the Czech Republic, PayU offers BNPL through an integration with local provider Twisto, which allows merchants to offer the option at checkout. Consumers receive an instant credit decision, and if approved, the order can be paid with a standard grace period of 30 days (extended up to 45 days for Twisto account users). PayU pays out the merchant the next day, and they assume responsibility for collecting payment from customers.

PayU’s innovative BNPL product offering is also available to Romanian shoppers using the eMAG platform. Bucharest-based online retailer eMAG is the first partner to offer its customers the possibility to either postpone a payment or to pay in four installments for all categories of products either in its own offer or for products sold by sellers active on the eMAG Marketplace. This facilitates greater diversity of payment choices and supports eMAG partners to grow their sales.

BNPL services are gaining a lot of traction across Africa driven by the combination of a digitally-savvy population, a mobile-first commercial mentality, and persistently high unbanked populations. BNPL offers merchants an opportunity to reach more population segments, such as the approximately 57% of Africa’s population (95 million people) who don’t have a traditional bank account.

In Africa, PayU can help merchants integrate BNPL through the payment methods offered via our payment gateway. Payflex, the first and largest BNPL player in South Africa, is one of many alternative credit payment methods offered by PayU in Africa, next to other names including Mobicred, Lulalend, and RCS.

Thanks to our partnership with Payflex, consumers in South Africa can now pay in four equal and interest-free installments, creating greater access to funding and autonomy on how consumers pay.

PayU’s recent launch of MoreTyme in partnership with Tyme Bank also allows customers of Tyme Bank to pay in three equal, interest-free installments. The checkout experience is simple, fast and frictionless since consumers don’t need to add their details. All they need to do is scan a QR code with their Tyme Bank app to complete the payment.

In addition to PayU’s payments business in India, we recently consolidated credit operations under our LazyPay brand, a direct consumer lender that offers a range of credit products from BNPL to personal consumer loans.

By introducing the ability to tap into innovative, accessible, and popular payment methods, PayU’s customers can provide a more streamlined and inclusive experience in their online shops.

These solutions were designed to give more consumers the opportunity to participate in e-commerce, while providing both local and global businesses with an opportunity to increase their reach and build customer loyalty.

BNPL is well on its way to disrupting the traditional pay-by-card model of consumer credit. As online shopping surges, BNPL continues to provide tech-savvy, money-conscious shoppers with a seamless payment alternative.

With e-commerce demand reaching new heights, merchants are seeking flexible solutions to address these expectations while easing financial pressures on their own businesses by avoiding chargeback fees. BNPL offers a unique win-win by enabling consumers to have more flexibility when it comes to making online purchases, while at the same time offering merchants the ability to expand their sales reach and convert more customers.

BNPL is here to stay. That’s why merchants looking to engage a wider range of customer segments – especially within younger generations – should ensure their buyers are offered the option to buy now and pay later as part of any checkout experience.