Having a basic knowledge of the entities involved in online payment processing is crucial when it comes to choosing the right payment provider for e-commerce.

As an e-commerce merchant, the difference between the various entities involved in accepting online payments is not always obvious.

Payment acquirers, payment processors, and payment service providers (PSPs) all play an essential role in facilitating the flow of online payments. But to businesses running an off-the-shelf payment gateway or who otherwise do not monitor their payments closely, it can be a challenge to untangle who does what when it comes to accepting payments.

As usual, with knowledge comes power: in this case, the power to increase revenue and profits by optimizing online payments.

In this article, we break down the difference between the various providers at different stages of the payment journey – and how you as a merchant can navigate the payment world to find the best option for your online business.

Payment processor vs. payment acquirer

What is a payment service provider (PSP)?

How can global merchants simplify the payment process?

The difference between payment acquirers and payment processors can be confusing to many newcomers. Some payment providers offer acquiring and processing as a combined service, muddling things up further. And people often use these two terms interchangeably, forgetting that they’re not the same thing.

It is important to understand that payment acquirers and payment processors are separate entities, although historically, they have been referred to as ‘the processor.’ Some financial institutions can be both payment acquirers and processors, but the fintech boom in recent years has shifted the industry toward using separate third-party processors.

Unlike a payment card acquirer that manages communications between banks and holds funds at various points, payment processors exist as a middle layer simply to process payments. Payment processors manage technical merchant services but don’t take on financial liability for it.

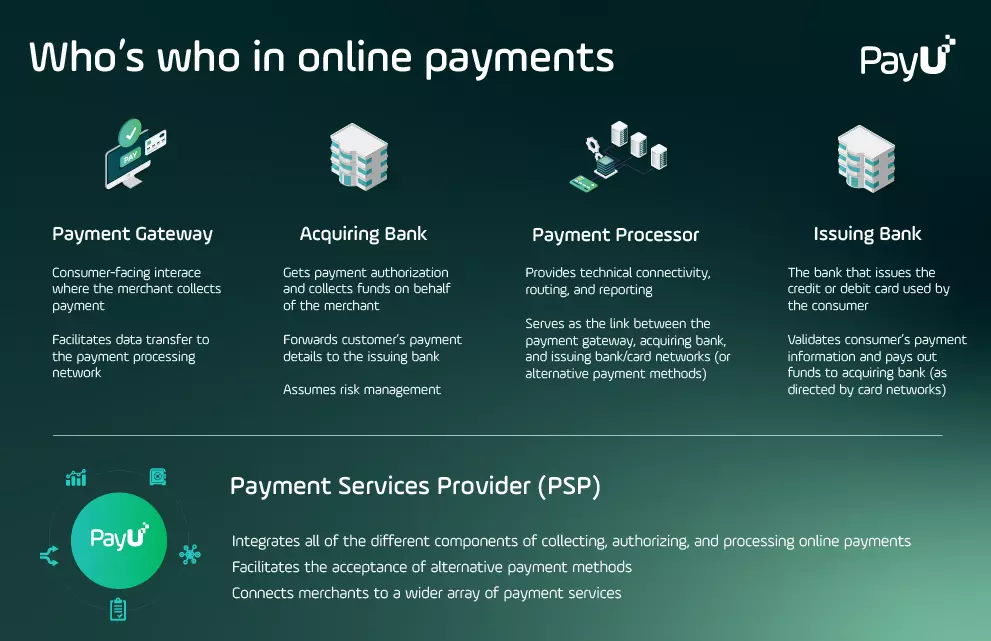

A payment acquirer (also commonly referred to as an acquiring bank) is a bank or other financial institution that processes credit and debit card payments for businesses.

It’s thanks to the payment acquirer that merchants can accept and process credit and debit card payments from card-issuing banks within a card association or scheme (such as Visa and Mastercard).

Once a transaction takes place, the merchant’s terminal (or payment gateway) forwards the customer’s payment details to the acquiring bank. The acquirer completes the transaction by running information through the card scheme to the card issuer to get authorization and complete the transaction.

Let’s examine this process:

But that’s not everything. Risk management, such as preventing fraud and illegal transactions, is also one of the key roles played by the payment acquirer within the card payments ecosystem. The acquiring bank takes full responsibility for their merchants and the transactions that they send to card schemes and issuers. The acquirer also deals with any chargebacks and/or disputes on any of their merchant’s transactions.

On the other side of the payments process, there’s an issuer – also known as the issuing bank. This entity is responsible for issuing cards to consumers with the major card schemes such as Visa, Mastercard, and American Express.

The payment processor serves as the link between the payment acquirer and the card schemes (or alternative payment methods) – providing technical connectivity, routing, and reporting services to acquirers and issuers.

When a transaction is approved, the payment processor also sends payment information to the payment acquirer so that they can forward funds to the merchant’s bank account.

Modern payment processors incorporate tokenization to increase the security of card transactions. When a customer enters their card information online, all data is sent through a payment gateway where it’s encrypted and turned into a token. Tokenization is a mechanism that replaces sensitive payment information with a non-sensitive equivalent, protecting it from theft, while transferring the responsibility for safeguarding the customer’s actual data from the merchant to the payment provider. The token is sent through the processor, which notifies the customer if the transaction has been approved or declined.

Merchants can take some steps to reduce payment declines in their business. For example, some payment providers allow merchants to set up custom routing rules which can send transactions to more than one payment processor. This results in fewer false payment failure messages and improves the e-commerce conversion rate.

So what distinguishes a payment processor from a payment service provider? The main difference is in scope.

PSPs connect merchants to a much wider array of payment services, helping to streamline the process of accepting and optimizing online payments.

Through a PSP a merchant can accept both credit and debit cards as well as alternative payment methods – including digital wallets such as Apple Pay, Google Pay, and PayPal, in addition to local payment methods unique to specific markets. Some PSPs provide merchant acquiring services, making the process much easier.

Many PSPs also provide merchants with an integrated payment gateway. As the consumer-facing interface where the customer enters their payment details via their preferred payment method, the payment gateway facilitates the communication and transfer of data to all of the different payment providers involved in a transaction. The payment gateway also determines which payment methods are available to the customer at the time of purchase.

It isn’t long before merchants operating in multiple markets discover that they have no choice but to add local payment acquirers, card networks, and alternative payment method providers to what is known as the “payment stack.” A payment stack refers to all of the financial layers that must interact with each other in order to enable a transaction.

As the facilitator connecting the customer checkout experience to everything going on behind the scenes, the payment gateway plays an integral role. Many aspiring global merchants find that they must work with different payment gateways in different markets, in order to accept payments in new locations. At the same time, they must do so continuously and fast to achieve scale.

The ability to accept payments in multiple markets through one global payment gateway is therefore an important part of growing business internationally. PSPs which offer an integrated payment gateway to merchants help facilitate seamless international expansion as well as an efficient approach to global payments.

Some of the benefits of having a global payment gateway include:

While dealing with multiple payment providers can be an obvious hassle for any online merchant, the situation becomes even more difficult when doing business across borders.

Merchants accustomed to using off-the-shelf payment gateway technology (such as that provided via popular e-commerce software providers like Shopify, Square, and others) can often overlook the complexities of the payment world when starting out, as payments are handled out of sight and out of mind through the webshop interface. But this solution doesn’t generally scale well – and there is no way to optimize payment traffic or gain insights into how much revenue might be lost due to false payment declines and other inefficiencies.

For businesses seeking to grow and achieve scale, payments will eventually become a critical piece of the puzzle. Rather than dealing with individual providers at each link in the payment process, merchants can work with a single PSP that consolidates all of the different payment layers under one provider.

While many PSPs operate at a regional level, companies like PayU offer global payment solutions that can allow merchants to accept payments in any market via one connection.

The payment gateway, the payment acquirer, the issuing bank, and the payment processor are all essential links in the journey of an e-commerce payment from the customer’s wallet to the merchant’s bank account. Many of these steps are referred to interchangeably, but they are unique components often handled by different providers.

In order to simplify the process of accepting online payments, particularly in multiple markets, lots of merchants choose to work with a payment services provider (or PSP) that can bundle everything together. PSPs make payments easier for the merchant, but not every PSP can offer global coverage or the ability to optimize payments.

The payment orchestration functionality provided by PayU combines all the capabilities of a traditional PSP along with advanced features such as fraud detection, real-time reporting, reconciliation, and more.

Merchants can also optimize their global operations with a platform that includes AI-based smart transaction routing, payment A/B testing, and many other tools for security and compliance.

Most importantly, PayU provides merchants with the capability to accept and optimize payments in any global market.

Get in touch with our team to see how your business can benefit from combining acquiring, payment processing, and all of the other payment components into one global solution for efficient e-commerce.