The right mix of online payment methods is one of the most important places to start when it comes to optimizing online revenue and conversions.

Keeping up with the latest payment trends is a prerequisite for merchants who want to provide a smooth checkout experience and increase their bottom line. Outdated payment solutions threaten businesses as they often lead to reduced conversions, unexpected technical issues, and a poor e-commerce experience.

Luckily, having a sophisticated online payment solution is now easier and more accessible than ever before – for businesses of all sizes.

Why should SMBs consider improving their payment capabilities?

In addition to paying lower fees in many cases, comprehensive payment solutions help minimize checkout friction, increase payment approval rates, and boost sales volume – all through one seamless integration.

One of the main benefits of upgrading payment technology is the ability to offer more online payment methods. A well-designed payment platform helps merchants easily integrate new global, local, and alternative payment methods, while providing additional payment security and optimization functionalities.

Which online payment methods should small businesses offer in order to keep up with the market? Keep reading to learn more.

Why expand your online payment capabilities?

The importance of offering the right online payment methods

Which online payment methods should SMBs offer?

What SMBs should look for when choosing a payment solution

Many small businesses can get by initially by using the payment functionality available in the e-commerce platform used to build and manage their online store.

But while this option tends to work out okay for companies just getting off the ground, as business grows payments inevitably become more complicated. New providers must be onboarded in order to process payments in some new markets. Other new markets might require payment methods that are not included in the payment gateway offered via the e-commerce platform. Security requirements increase.

Finally, off-the-shelf payment technologies do not provide the same outing and optimization capabilities as a dedicated payment solution – capabilities that could be worth tens of thousands or more in optimized revenue and e-commerce margins.

Another story is the transition merchants make during their digital transformation journey. By digitizing payments and optimizing processes, small companies can significantly reduce the administrative burden on their business – saving both time and money in the process. Many SMBs accepting payments online do so through sub-optimal processes that leave value on the table when it comes to reconciliation, settlement, and other stages of the online payment processing journey.

The e-commerce landscape is ever changing – and impacting customer expectations along with it. To keep up, small businesses must stay focused on delivering a seamless online shopping and checkout experience.

And while this might not be a new statement for many e-commerce entrepreneurs, some are not aware of the importance of online payment methods when it comes to driving e-commerce conversions and revenue.

The right mix of online payment methods help merchants reach more customers, increase conversions, reduce cart abandonments, and even boost payment approval rates. When expanding to new markets, payment methods are an important part of localizing a merchant’s online presence.

Many off-the-shelf payment technologies offer only generic payment methods – which may not fully capture local credit card providers, banks, e-wallets, BNPL, and other payment methods that could be an important part of the consumer mix in a given market.

Customers who reach the checkout page and don’t see their preferred payment method are more likely to abandon the transaction altogether. Payment methods are thus a critical part of ensuring maximum e-commerce performance.

Credit cards are still one of the most important payment methods in e-commerce. Most payment gateway technology supports the major global credit cards, but the situation becomes more interesting in local markets. In particular, local credit card issuers play an important role in the e-commerce landscape of many emerging markets.

Depending on the payment provider, card payments may come with relatively high transaction fees. Another common issue merchants face is the high payment failure rate due to lost and expired cards. This naturally results in lost customers and lost revenue.

Another challenge is the importance of safeguarding customer card data, governed by the PCI-DSS standard. This can result in heavy fines for merchants if not done correctly.

The right payment solution can help businesses process card payments more efficiently, while safeguarding customer data via tokenization, thereby lowering the merchant’s responsibility or “PCI scope” when it comes to handling customer card details.

Consumers find direct debits very convenient and merchants often use this online payment method to set up recurring automated payments. Any small business based on a subscription model benefits from this option.

The most significant advantage of direct debit payments is that payment is almost instant, so there’s no need to wait for customers to pay an outstanding invoice. This is also convenient for customers as they don’t have to approve payments when their debit card is used for recurring payments.

With direct debit, the payment provider automatically takes funds from the customer account once the merchant sets up the direct debit payment method.

An e-wallet or digital wallet is a type of software that stores information for different payment methods, along with other items such as boarding passes, gift cards, or driver’s licenses.

Accepting e-wallet payments reduces cart abandonment and increases trust, especially when using wallets with high brand name recognition, such as Google Pay or Apple Pay. In such scenarios, the digital wallet access uses the shopper’s device, potentially secured with facial IDs, thumbprints, and security codes. This leads to a lower risk of fraud for merchants.

To make this type of payment work, merchants need to accept the right wallet in each market, which is challenging given the number of wallets available worldwide.

Integrating with multiple e-wallets is often time-consuming and expensive. This is why many merchants turn to an all-in-one payment solution in order to accept e-wallets.

Mobile payments encompass mobile wallets as well as mobile money transfers, helping merchants to offer an alternative way of paying for goods or services that is less expensive for businesses than accepting credit card payments.

Accepting mobile payments allows small business owners to make payments more convenient for customers. This payment method also opens the door to integrating loyalty and reward programs, serving as a great source of data for customer analytics.

Payment security is a key concern in this area, leading businesses to choose payment providers offering comprehensive mobile payment solutions.

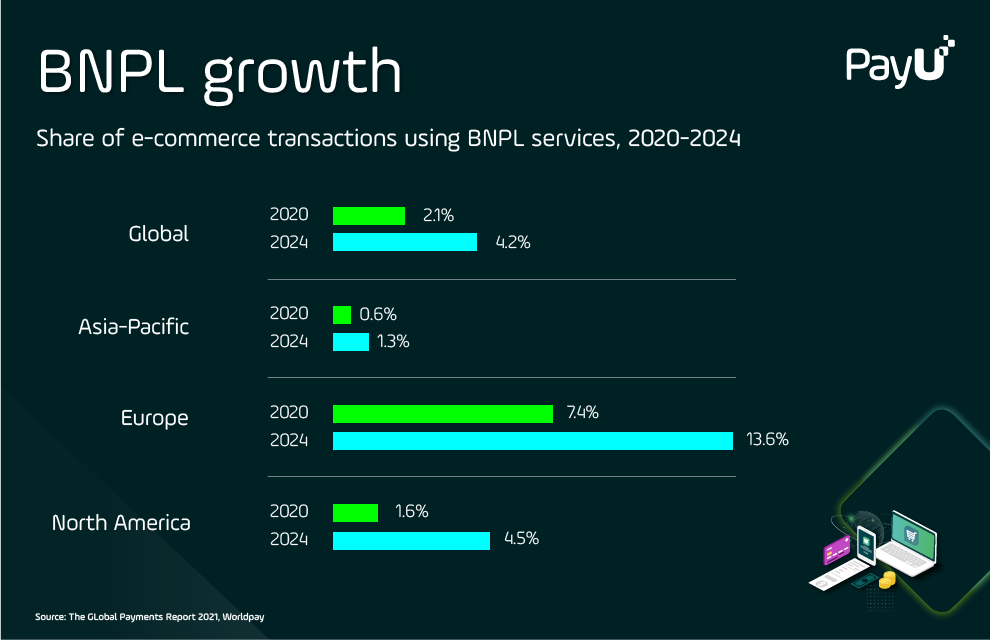

BNPL payments allow merchants to be paid upfront before customers pay for the transaction. In this scenario, the provider fronts the transaction amount and takes on any risk of fraud or delay.

Because it can help customers to feel more comfortable making a larger purchase, BNPL usually results in higher transaction values and conversion rates at checkout. For longer installment cycles, BNPL models take advantage of predictive algorithms that provide instant credit decisions as part of the checkout process.

In many emerging markets, BNPL serves as a means of financial inclusion, enabling more people to participate in the digital economy. Of the more established global e-commerce markets, BNPL is particularly popular in Europe – especially in countries such as Germany, Scandinavia, Austria, Switzerland, and the Netherlands.

For many small businesses operating with limited staff or budgetary resources, convenience and efficiency are a key consideration when choosing any external supplier. The same goes for a payment provider.

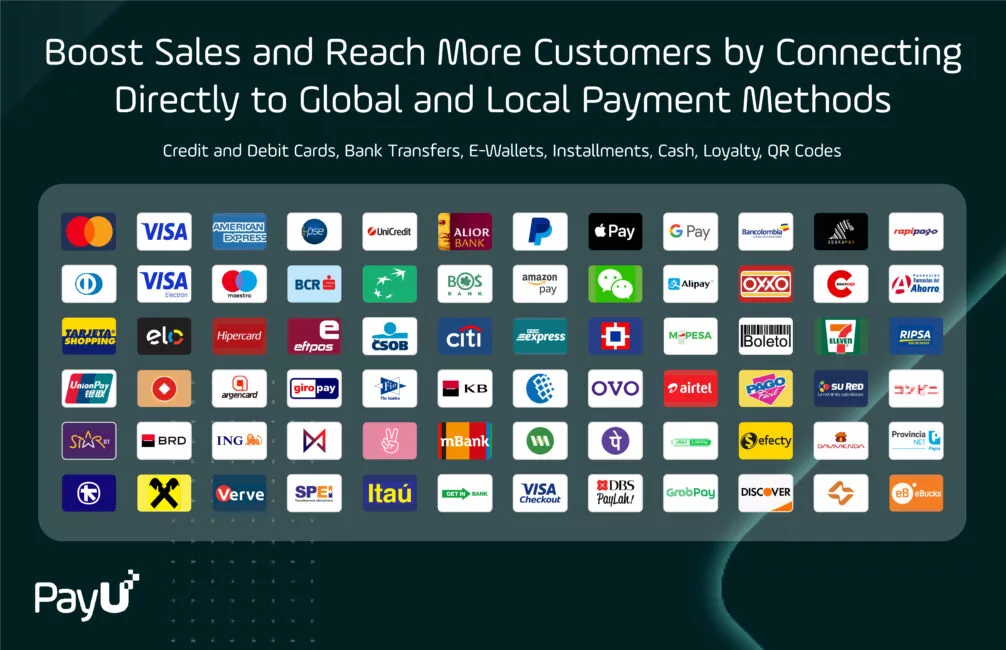

To help small businesses expand their operations and reach new customers around the world, PayU has developed a solution that allows merchants to quickly and easily get onboarded to some of our most important local payment platforms.

A few steps are all that’s needed to integrate the merchant’s store with our local payment processing platform.

For companies interested in offering a more tailored mix of local and alternative payment methods to customers, a piecemeal approach can quickly become cumbersome. Adding individual new payment methods, or even clusters of payment methods, might require onboarding multiple new payment processing partners on a local or regional basis. The cost and administrative burden of this can quickly add up.

But this doesn’t have to be the end of the story. One way for companies to achieve maximum reach when it comes to payment methods is to work with a global payment solution provider, who can offer hundreds of payment methods around the world via a single integration. The global provider connects merchants to local processing networks and acquiring banks as required, so that the merchant does not have to do so themselves.

PayU, as an example, is able to offer a mix of global, local, and alternative payment methods tailored to any market, through a mix of our own local platforms as well as those of our partners.

What is local expertise in payments? It’s the ability to leverage specific-to-market and popular local payment methods, along with the insights that go along with this.

To take a European example: online shoppers in Poland prefer using local payment methods such as BLIK, bank transfers, open banking payments, installment payments, cards, and e-wallets.

Just to the south, Romania has a completely different e-commerce landscape. Local customers there prefer to use free installments offered from local banks, as well as credit card payments with all the local banks.

The situation becomes even more complex when merchants start exploring countries on other continents. For example, merchants using PayU’s platform in Colombia can access more than 12 million online shoppers using a variety of local and alternative payment method options: Pagos Seguros en Línea PSE (the number one alternative payment method in Colombia), Codensa (a popular local credit card not supported by many providers), or via a variety of local e-wallets and alternative payment methods.

In Colombia and across Latin America, cash voucher schemes are another highly prevalent local payment method. This payment method allows shoppers without a bank account or credit to shop online by checking out with a digital voucher, which can then be paid in cash at a network of participating brick-and-mortar retail locations. It’s thus an important tool for digital and financial inclusion, by enabling the region’s large unbanked population to still be able to access e-commerce.

Another aspect merchants should take into account when choosing a payment provider is whether the payment solution has been tailored to a given region.

Looking again at Latin America, PayU’s solution has been designed to comply with local regulations that require the step of identity and banking validation from merchants based in the region. Business owners in other regions can do this via an automatic penny transfer.

It’s key for the payment processor to be able to navigate these regional differences and ensure that their solution achieves compliance and mitigates security risks for merchants.

Small businesses have more opportunities than ever to scale their business by reaching global customers. But the right mix of payment methods is important for ensuring that this growth is a success.

The choice of which payment methods to offer will depend on a merchant’s business model, target market, and the customer preferences within those markets. The best payment solution for a small business should be easy to integrate, affordable, and capable of integrating with other software merchants might use for their business operations.

By choosing a payment provider with global reach, SMBs can efficiently tap into hundreds of payment methods and ensure they are prepared to sell in any global market. At the same time, dedicated payment solution providers can also ensure more efficient payment processing at the local level, capturing more value by driving higher conversion and approval rates, increasing revenue, and achieving better margins.