How can merchants achieve higher approval rates and lower transaction fees in online payment processing? Take a look at what’s going on behind the scenes of an online payment.

In our e-commerce era, expectations for speed and convenience when shopping online mean that the process of checking out must be as easy as possible for the end user. Consumers expect seamlessness and efficiency while paying for goods online. What’s more, the bar is being raised all the time. Companies that struggle to deliver a convenient payment experience risk losing out on existing and potential future customers.

However, frictionless payments involve a lot more than the customer simply adding their payment details and clicking the “Pay Now” button.

Take a look behind the scenes of any online payment and you’ll find a maze made up of multiple interconnected players that must be coordinated to deliver a speedy and successful transaction. Each has a role in making sure that transactions are carried out smoothly and to the satisfaction of both merchants and their end customers.

How can merchants ensure that payments are as efficient as possible – while optimizing for key metrics like transaction costs and payment approval rates that can make a big difference when it comes to e-commerce revenue?

Keep on reading to learn more about the technicalities of online payment processing – and how merchants can optimize the process by coordinating the different pieces together.

What is a Payment Processor/Payment Facilitator?

Key Players in Online Payment Processing

How Payment Processing Works: A Step-by-Step Guide

Which Types of Online Payments are Processed?

Tips to Optimize Online Payments

How to Choose a Payment Processor that Can Optimize Online Payments

To understand how online payments can be optimized, it’s helpful to review what a payment processor is responsible for, and how this can support (or hinder) frictionless online payments.

A payment processor, sometimes also called a payment facilitator, acts as a middle layer between the merchant and the financial institutions on both sides of an online transactions. The payment processor works between both side to authorize transactions and ensure the safe transfer of funds.

Companies that deliver payment processing services perform multiple steps required to authenticate and settle transactions, ensuring that the payment is approved and that the merchant is paid out.

Here are a few of the responsibilities that fall onto the shoulders of online payment processing providers:

Here is an overview of the key players involved in online payment processing – and the technology linking them together.

A business selling products or services using a website or mobile app.

Users who go through a checkout flow to purchase item(s) or pay for services online.

During an online transaction, two key technologies facilitate the flow of payments between merchant and buyer:

The payment gateway is a software which connects the checkout page/shopping cart on a merchant’s website to the payment processing network. This is the visible interface that the customer sees when making a payment. The payment gateway is responsible for encrypting the buyer’s data and then forwarding it to the payment processor – who does all the work behind the scenes to complete the transaction.

The payment processor coordinates between the different intermediaries involved in ensuring a successful payment. For card payments, there are three main players: the issuing bank (the bank responsible for the cardholder’s funds); the acquiring bank (the merchant’s bank account); and the credit card network. For bank transfers and other alternative payment methods like e-wallets or Buy Now Pay Later (BNPL), the payment processor facilitates directly between the payment method provider and the acquiring bank. The main jobs of the payment processor include:

In order to optimize online payments it’s helpful to understand how exactly money moves from the customer to the merchant.

There are two main stages to payment processing: authorization (approving the sale) and then clearing and settlement (getting the money into the merchant’s account).

Let’s dive in.

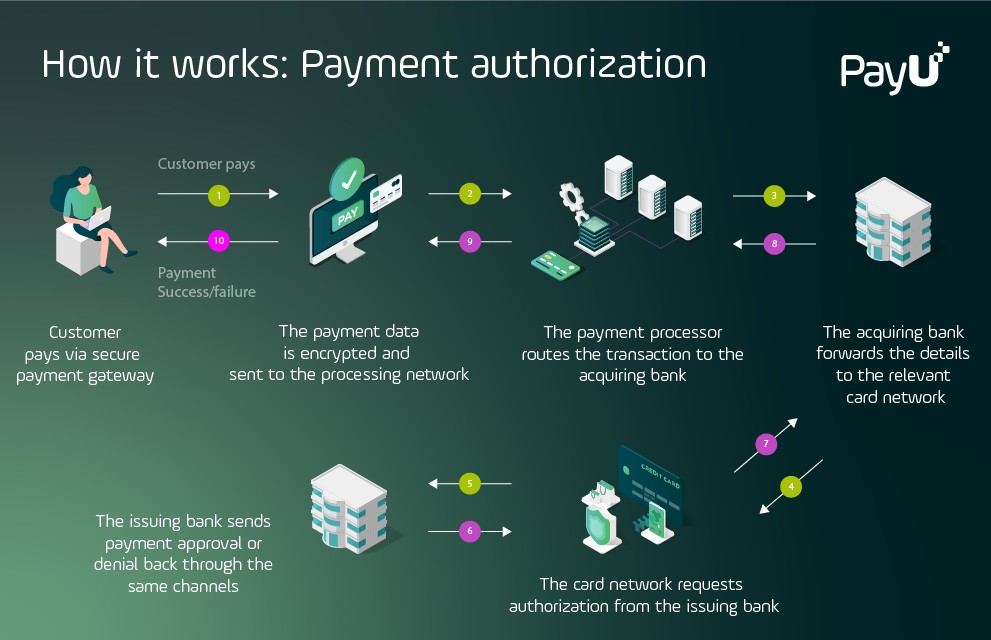

Authorization is the process of verifying that the payment information is legitimate and that the buyer’s account has sufficient funds, before placing a temporary hold on those funds.

The following stages are commonly followed during the authorization of a card payment:

Amazingly, all of the above takes place within a few seconds.

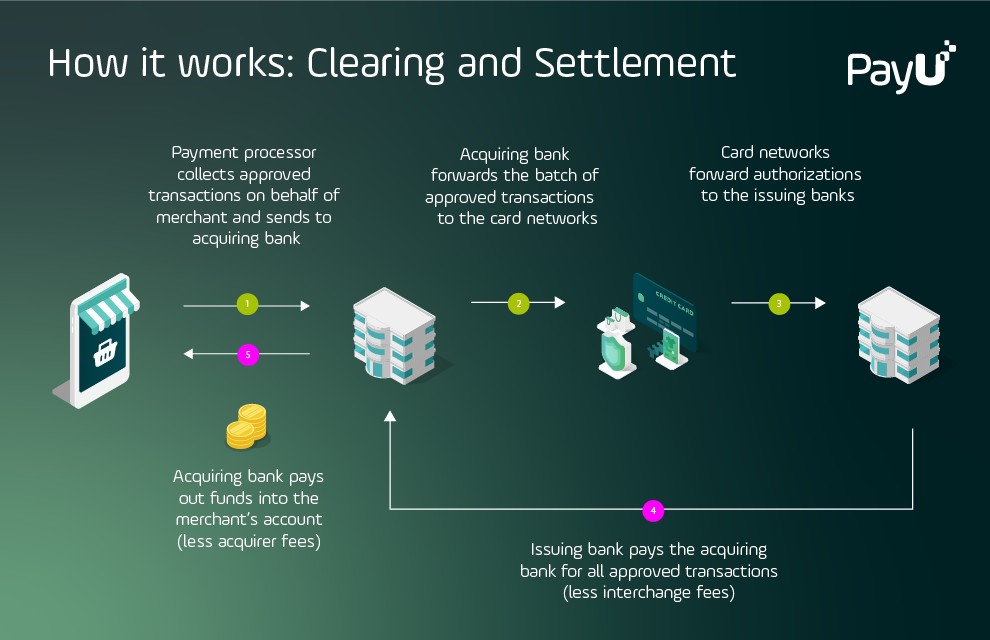

Clearing is the process of finalizing and posting the transaction to the cardholder’s account. A capture request from the merchant bank initiates this procedure. Once a transaction has been cleared, the process of transferring payments to the merchant’s bank from that of the cardholder is known as settlement. Here’s an overview of how it all works in real-time:

It can take up to a few days to complete the settlement process. In some cases, the merchant’s bank may allow the merchant to access the funds before they are fully settled.

They may also store a percentage of the money in the merchant’s account in case the buyer returns something later (this is called a reserve in payment industry terms).

In addition to card payments, a good payment processor should allow merchants to accept a broad range of additional online payment methods from their customers. Here are some examples of popular payments methods today:

This one is still a favorite among many consumers. Although credit cards have long been the dominant form of payment in most established e-commerce markets, in many countries the landscape is now changing as e-wallets, BNPL, and other alternative payment methods chip away at card market share.

In many European countries where consumers do not have or typically use a credit card, bank account transfers are the most common form of e-commerce payment.

E-wallets allow customers to store and access payment information digitally, and can be used either with their own balance or as a “pass-through” in combination with a credit card or bank account. Much of the visibility when it comes to e-wallets in North America and Europe tends to go to big names such as PayPal as well as the native e-wallet products from Apple, Amazon, and Google. But this is only one part of the picture.

Most merchants have heard of AliPay or WeChat, which dominate the market in Asia. Many other countries, however, are full of local e-wallet brands which global merchants may not have even heard of, but which are some of the most popular and important forms of payment in their local markets.

Bank transfers enable e-commerce customers to pay for goods by sending money from one bank account to another. The infrastructure underpinning account-to-account payments differs between countries and regions, but the concept is the same in that the buyer is making a direct transfer to the merchant’s bank account (sometimes through an intermediary).

Similarly to e-wallets, local markets have their own popular local banking products when it comes to e-commerce – which are important for merchants to be able to offer as a local payment method option.

What exactly is referred to as an alternative payment method (or APM) can fall under a large umbrella. In general, alternative payment methods encompass anything that isn’t cash or a major credit card. More specifically, APMs can refer to the many specialized payment methods that also fall outside of mainstream e-wallets and banking services.

Examples include the emerging landscape of Buy Now Pay Later (BNPL) payment methods, mobile services, and local e-wallets as well as cash voucher payment methods. The latter tend to be particularly popular in emerging markets with large unbanked populations. The customer completes a transaction online and then receives a code to pay for their goods in cash at a participating retail location. Once payment has been completed, the goods are delivered.

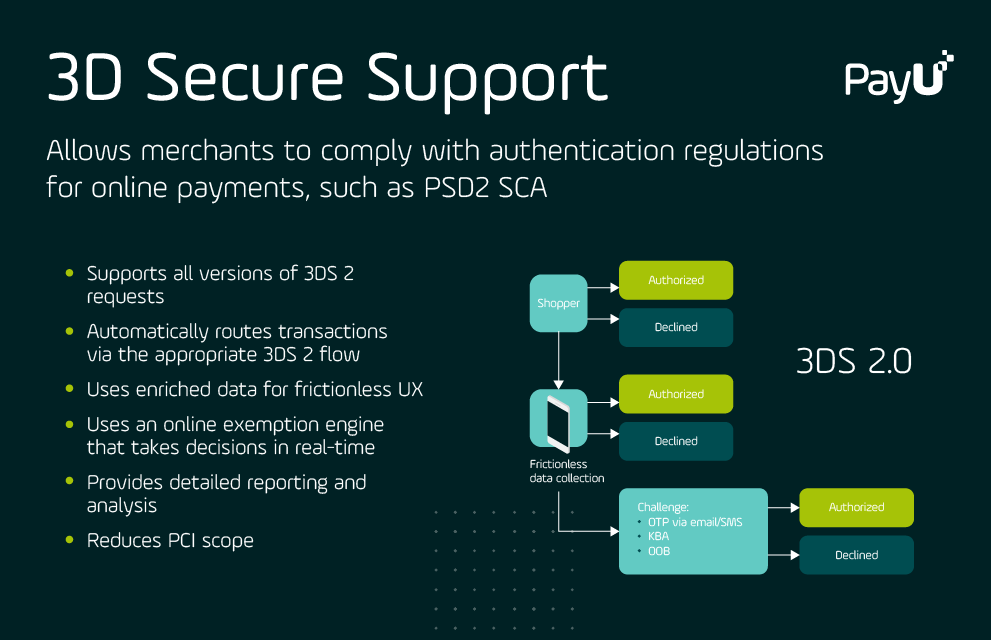

Open Banking is a safe way for customers to access third-party financial services through a direct connection with their bank. Open banking unites banks, third-parties, and technological suppliers, allowing them to exchange data easily and securely for the benefit of their consumers.

As the global e-commerce landscape continues to develop and diversify, open banking is growing more popular since it allows for faster, more secure transactions from anywhere in the world – while also providing consumers with more financial options. Banks and many companies in Europe, for example, are already making use of Open Banking since the rollout of the European Union Second Payment Services Directive, or PSD2. This piece of EU payments law took effect in September 2019 and aims to improve digital payments capabilities while giving customers more control over their financial data.

Merchants often find it challenging to strike a balance between maintaining high payment approval rates and optimizing transaction processing costs.

By adopting the following best practices, merchants can increase approval rates and lower the costs of processing payments.

The success or failure of a given transaction can vary widely based on a number of criteria including the payment method or card type used, the transaction amount, the time, risk level, and more. In the increasingly global world of e-commerce, no single payment processor can guarantee that they will be able to provide the same results every time.

For a specific sort of transaction (e.g. payments with a global credit card from more established e-commerce markets), one supplier may be able to offer faster processing, higher approval rates, and lower costs. Yet that same supplier may struggle to deliver equally satisfactory outcomes for the same transaction if it takes place in another geography with different local banks and payment methods in the mix.

To get the best results when it comes to payments, merchants should have a diverse portfolio of payment processing providers, both locally and globally. However, a multi-provider structure poses certain challenges – particularly for administration and efficiency, as well as payment optimization.

The good news is that there are options for dealing with this problem. A good place to start is the payment gateway platform. A high-quality, customizable payment gateway can provide merchants with a single, direct connection to multiple payment processing services and a wider variety of local and global online payment methods.

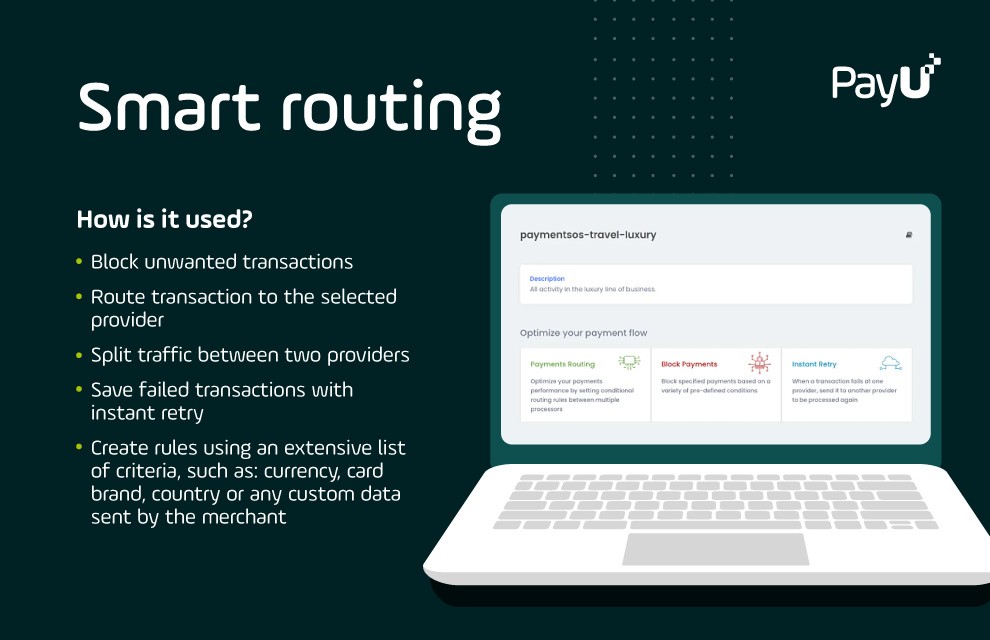

To increase payment approvals, merchants should look for payment providers who use advanced configurable features for optimizing payment traffic. Examples include:

Customers are passionate about their payment preferences and typically will spend more when a merchant offers their preferred payment method. In some markets, common global payment methods are not widely used or widely accessible. At the same time, in other markets there are payment methods which only exist locally yet are among the most popular and standard forms of payment.

Merchants benefit from offering the right payment methods to reach a broader audience of end customers.

Offering a variety of global and popular local payment methods such as BNPL, e-wallets, and other popular alternative payment methods improve conversions both at the local as well as the global level.

In relation to the first tip (working with multiple providers and acquirers): having a global interface for acquiring means not needing to manage local acquirers or multiple providers for different types of payments.

This global to local approach allows merchants to process payments with acquiring banks in the same market as the cardholder, which can provide merchants with a competitive advantage by resulting in higher approval rates, lower transaction fees, and faster settlement in each market.

By implementing a global strategy, merchants can realize the benefits of local processing without needing to work with individual payment processors in each local market.

Merchants need best-in-class tools to fight fraud and separate legitimate transactions from the illegitimate that help protect against data breaches and keep both them and their customers secure. Key elements include:

From a merchant’s perspective, implementing the above best practices allows for a variety of improvements that increase payment performance and e-commerce success.

Offering more payment methods helps merchants to localize their product offering by localizing the checkout experience.

At the same time, by processing payments locally, merchants benefit from higher approval rates and lower fees.

By working with a global payment facilitator who can provide access to local payment processing services, merchants get the best of both worlds – the benefits of local payment methods and local payment processing, combined with the efficiency of one provider and the opportunities for payment optimization and security that come with having a single global solution.

Most online merchants are familiar with the basic necessities for accepting online payments – beginning with the payment gateway. Merchants using services like Shopify, Wix, and other off-the-shelf e-commerce technology typically have access to an integrated payment gateway through their chosen webshop provider. But this provides only limited functionality.

For merchants seeking to optimize their online payments, or who need to accept payments in a wider range of global markets, it’s a good idea to consider working with a partner who can deliver multiple integrated payment services.

Here are some examples of typical value-added services to look for which can optimize the processing of online payments:

When choosing a payment provider, check if it supports the major credit card networks and popular e-wallets. Make sure that it also offers a broad range of local payment methods if you’re planning to target specific geographic locations, and alternative payment methods beyond just the typical global e-wallets and bank transfers.

At the same time as customers expect to see a variety of payment method options upon checkout, local and alternative payment methods are also one way to increase approval rates, lower transaction costs, and battle false declines. In addition to carrying lower fees, in most cases local payments have a better chance of getting approved and are less likely to trigger fraud filters.

For these reasons, choosing a payment provider with global reach can be a smart move. PayU allows merchants to sell anywhere in the world through one platform while offering hundreds of local, global, and alternative payment methods tailored to the needs of individual markets.

Next, merchants should check whether their online payment processing company meets the Payment Card Industry Data Security Standard (PCI DSS). PCI DSS applies to anyone that handles user credit card data, and is governed by over 400 sub-requirements and test procedures based on each party’s level of data handling or “PCI scope”.

In the payment world, security goes hand in hand with compliance. Incorporating key security features into your payment provider is the best way to stay compliant with PCI and other industry standards.

PayU leverages our status as a PCI Level 1-certified online payment processor to deliver industry-leading payment security as part of our global payment offering.

Merchants can benefit from multiple levels of AI and automation when it comes to managing payments. Automated tools are a must-have for managing payments and help merchants boost customer retention.

At the same time, innovative AI-based functionalities like instant retry and intelligent routing can help merchants lower costs and boost approval rates by sending payments through the optimal combination of global providers. PayU’s Smart Routing Engine holds a US patent and gives merchants the opportunity to establish customized routing rules that can also block unwanted transactions.

With so many parties involved in each global transaction, it can be a challenge to find efficiencies when working with too many payment providers at once. PayU offers an advanced payment technology stack with a quick onboarding of just a few minutes to set-up the platform.

In addition to benefiting from tools like smart routing, a good way to limit excess transaction costs is to use one global payment solution that can deliver the full payment package at scale and offer lower costs on each payment.

PayU offers a global acquiring strategy with a local approach resulting in higher authorization rates, lower transaction fees, and faster settlement in each market.

While payments are designed to seem straightforward to the end user, and might even be an afterthought for most merchants, many global e-commerce businesses find that they are leaving a significant amount of money on the table due to high payment transaction costs, low approval rates (which can be a challenge particularly in more emerging e-commerce markets), and other inefficiencies.

To optimize online payment processing, local and global businesses alike should consider their payment strategy – while looking for a global payment partner with the technologies and services available to improve payment performance each step of the way.